Teck Resources Limited

TECK

recently provided fourth-quarter and 2021 sales and production results citing effects of logistics disruptions in British Columbia (B.C), Canada.

Steelmaking coal is benefiting from strong demand from steelmakers with free on board (FOB) price increasing from $356 per ton at the end of December to $445 per ton. Additionally, record-high clean coal inventory levels at its mines are likely to translate to higher sales exceeding production by 1.2 to 1.5 million tons in the current year. Consequently, higher prices and increased sales volumes will likely generate strong cash flow in the first half of 2022. Realized average steelmaking coal prices in the fourth quarter were $351 per ton, up from $277 per ton in third-quarter 2021.

Extreme cold weather, heavy rainfall, flooding and landslides in B.C coupled with previously-occurred forest fires incident in the country affected the company’s rail service and logistics operations since mid-November. This scenario persisted till mid-January as adverse weather conditions have continued to impact recovery efforts in B.C operations. Resulting which, Teck’s realized steelmaking coal sales were 5.1 million tons during the fourth quarter, slightly below the low end of its prior guidance of 5.2 to 5.7 million tons. The company expects to significantly recover delayed fourth-quarter sales in the first half of the current year. Steelmaking coal production was 24.6 million tons in 2021, within its prior guidance of 24.5-25 million tons.

During the fourth quarter, Teck incurred $72 per ton adjusted site cash cost of sales and $49 per ton of transportation costs, which were above the upper range of its annual guidance. Ongoing logistics challenges and inflationary pressures drove these costs higher.

While the logistics interruptions had a nominal impact on Highland Valley Copper (HVC) production, sales of copper concentrate from HVC operation were 5,600 tons lower than production in the December-end quarter. This deficit was partially offset by strong sales at Teck’s other operations.

Teck’s guidance reflects uncertainties related to the extent and impact of the COVID-19 pandemic on demand as well as commodity prices, suppliers and global financial markets. The recent spike in cases with the Omicron COVID-19 variant might unfavorably impact Teck’s operations in the near term. Moreover, steelmaking coal operations in the Elk Valley operation in first-quarter 2022 might be impacted by a rising number of omicron cases in southeastern B.C. The company’s Quebrada Blanca Phase 2 (QB2) copper project has made strong progress in the October-December quarter despite increasing COVID-19 cases in Chile. The project is likely to start in the second half of 2022. COVID-19 related capital cost will continue to impact QB2 construction, which is expected in between $900 million and $1,100 million, up from the prior estimate of $600 million. The company is bearing the brunt of inflationary cost pressures, particularly in diesel prices, supplies and labor costs. These are likely to continue in the current year as well.

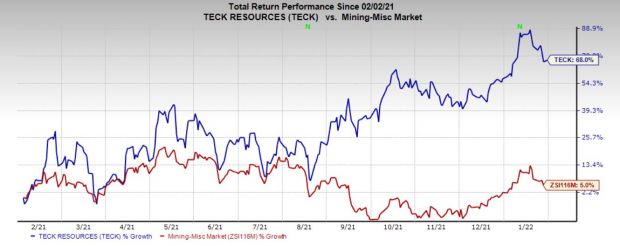

Price Performance

Teck’s shares have gained 68% in the past year, compared with the

industry

’s growth of 5%.

Image Source: Zacks Investment Research

Zacks Rank & Stocks to Consider

Teck currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks from the basic materials space are

Commercial Metals Company

CMC

,

Haynes International, Inc.

HAYN

and

AdvanSix Inc.

ASIX

. Each carrying a Zacks Rank #1 (Strong Buy) at present. You can see

the complete list of today’s Zacks #1 Rank stocks here.

Commercial Metals has an expected earnings growth rate of 10.5% for the current fiscal year. The Zacks Consensus Estimate for CMC’s current-year earnings has been revised 6.6% upward in the past 60 days.

Commercial Metals’ earnings beat the Zacks Consensus Estimate in three of the trailing four quarters and missed once, the average being 7.4%. CMC has gained 69% over a year.

Haynes has an expected earnings growth rate of 298.6% for fiscal 2022. The Zacks Consensus Estimate for fiscal 2022 earnings has been revised 53.2% upward in the past 60 days.

Haynes’ bottom line beat the Zacks Consensus Estimate in three of the trailing four quarters, the average surprise being 83.1%. HAYN has rallied 76.7% over a year.

AdvanSix has an expected earnings growth rate of 194.5% for the current year. The Zacks Consensus Estimate for current-year earnings has moved 14.1% north in the past 60 days.

AdvanSix’s bottom line beat the Zacks Consensus Estimate in each of the trailing four quarters, the average being 47%. ASIX has soared 127.6% over a year.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +25.3% per year. So be sure to give these hand-picked 7 your immediate attention.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report