Kamoa-Kakula copper joint venture in the Democratic Republic of Congo sold 53,165 tonnes of payable copper and recognized revenue of $488.5 million in Q4 2021

Kamoa-Kakula recorded operating profit of $198.9 million and an EBITDA of $357.6 million for the fourth quarter

Kamoa-Kakula’s cost of sales total $1.12 per pound of payable copper in Q4 2021, with C1 cash costs of $1.28 per pound

Kamoa-Kakula’s Phase 2 expansion on track to begin operations in April 2022, doubling the size of the mine’s concentrator plant

Kamoa-Kakula positioned to be the world’s fourth largest copper producer by Q2 2023, with projected annual copper output of more than 450,000 tonnes

Construction of Ivanhoe’s Tier-One Platreef palladium, rhodium, nickel, platinum, copper and gold project in South Africa advancing to first production in Q3 2024

New agreement signed to return the ultra-high-grade Kipushi Mine in the Democratic Republic of Congo to commercial production

Toronto, Ontario–(Newsfile Corp. – March 8, 2022) – Ivanhoe Mines (TSX: IVN) (OTCQX: IVPAF) today announced its financial results for the year ended December 31, 2021. Ivanhoe Mines is a leading Canadian mining company developing and expanding its four principal mining and exploration projects in Southern Africa: the Kamoa-Kakula copper mining complex in the Democratic Republic of Congo (DRC) that began commercial operations in July 2021; the Platreef palladium, rhodium, nickel, platinum, copper and gold discovery in South Africa; the historic Kipushi zinc-copper-lead-germanium mine in the DRC; and the expansive exploration program for new copper discoveries on Ivanhoe’s Western Foreland exploration licences, near Kamoa-Kakula. All figures are in U.S. dollars unless otherwise stated.

HIGHLIGHTS

-

Ivanhoe Mines recorded a profit of $48.2 million for Q4 2021, compared to a loss of $10.9 million for the same period in 2020. Ivanhoe Mines’ share of profit from the Kamoa-Kakula copper joint venture (Kamoa Holding) and finance income of $103.9 million were the principal contributors to the profit recorded in the fourth quarter.

-

The Kamoa-Kakula Mining Complex produced 54,481 tonnes of copper in concentrate in Q4 2021, compared to 41,545 tonnes produced in Q3 2021.

-

Kamoa-Kakula produced a total of 105,884 tonnes of copper in concentrate in 2021, significantly exceeding the initial 2021 production guidance range of 80,000 to 95,000 tonnes, as well as the increased guidance of 92,500 to 100,000 tonnes for 2021.

-

Kamoa-Kakula’s copper recoveries increased from an average of 81% in July 2021 to a record of 88.5% in December 2021. The Phase 1, steady-state-design copper recovery is approximately 86%, depending on ore feed grade.

-

During Q4 2021, Kamoa-Kakula sold 53,165 tonnes of payable copper and recognized revenue of $488.5 million, with operating profit of $198.9 million and EBITDA of $357.6 million.

-

Kamoa-Kakula’s cost of sales per pound (lb) of payable copper sold was $1.12/lb for Q4 2021, while cash costs (C1) per pound of payable copper produced totalled $1.28/lb; compared to $1.08/lb and $1.37/lb in Q3 2021, respectively. Cash costs are expected to continue to trend down as the Phase 2 concentrator plant is commissioned and the mine’s fixed operating costs are spread over increased copper production.

-

Kamoa-Kakula’s Phase 2 concentrator plant is on track to begin operations in April 2022, which will see a doubling of Kamoa-Kakula’s nameplate milling capacity throughput to 7.6 million tonnes of ore per annum (Mtpa).

-

A de-bottlenecking program is underway to expand processing capacity of the Phase 1 and Phase 2 concentrators by 21%, to a combined total of 9.2 million tonnes of ore per year. The de-bottlenecking program is projected to boost copper production from Kamoa-Kakula’s first two phases to more than 450,000 tonnes per year by Q2 2023, positioning Kamoa-Kakula as the world’s fourth largest copper producer.

-

Ivanhoe Mines has a strong balance sheet with cash and cash equivalents of $608.2 million as at December 31, 2021, and expects that the majority of Kamoa-Kakula’s expansion capital expenditures on Phase 2 and Phase 3 will be funded from copper sales and project facilities already in place. Based on current market conditions, it is expected that Ivanhoe Mines will start to receive shareholder loan repayments from Kamoa-Kakula in 2022.

-

During Q4 2021, Ivanhoe continued its copper exploration program on its Western Foreland licences that cover approximately 2,550 square kilometres in close proximity to Kamoa-Kakula. An extensive drilling program is planned for 2022, commencing with the onset of the dry season in the DRC, which will build upon Ivanhoe Mines’ 2021 work program that was focused on airborne and ground-based geophysics, soil sampling and road construction.

-

Exploration models that successfully led to the discoveries of Kakula, Kakula West, and the Kamoa North Bonanza Zone on the Kamoa-Kakula joint-venture mining licence are being applied to the extensive Western Foreland land package by the team of exploration geologists responsible for the previous discoveries.

-

In December 2021, the Platreef Project secured a $200-million gold stream financing and additional $100-million palladium and platinum stream financing, with the first prepayment of $75 million received in December 2021.

-

In February 2022, Ivanhoe Mines announced the outstanding results of a new independent feasibility study for the Platreef Project that builds on the alternate scenario to expedite production, based on a steady-state production rate of 5.2 Mtpa, confirming the viability of a new phased-development pathway to fast-track Platreef into production in Q3 2024.

-

Platreef feasibility study’s sensitivity analysis at current metal prices of approximately $1,121/oz platinum, $2,979/oz palladium, $22,200/oz rhodium, $1,995/oz gold, $4.84/lb copper and $13.12/lb nickel (March 7, 2022), results in an after-tax NPV8% of $5.1 billion with an after-tax real IRR of 33%.

-

In February 2022, Ivanhoe Mines and Gécamines signed a new agreement to return the ultra-high-grade Kipushi Mine back to commercial production.

-

In February 2022, Ivanhoe Mines announced the positive findings of an independent feasibility study for the planned resumption of commercial production at Kipushi based on a two-year construction timeline. Kipushi feasibility study’s sensitivity analysis at current zinc prices of approximately $1.84/lb (March 7, 2022), results in an after-tax NPV8% of $3.0 billion with an after-tax real IRR of 86%.

-

At the end of 2021, Kamoa-Kakula had reached 2.7 million work hours free of a lost-time injury, Kipushi had reached approximately 4.0 million work hours free of a lost-time injury, and Platreef had reached 677,450 work hours free of a lost-time injury.

Principal projects and review of activities

1. Kamoa-Kakula Mining Complex

39.6%-owned by Ivanhoe Mines

Democratic Republic of Congo

The Kamoa-Kakula Mining Complex, a joint venture between Ivanhoe Mines and Zijin Mining, has been independently ranked as the world’s fourth-largest copper deposit by international mining consultant Wood Mackenzie. The project is approximately 25 kilometres west of the town of Kolwezi and about 270 kilometres west of Lubumbashi. Kamoa-Kakula began producing copper in May 2021 and achieved commercial production on July 1, 2021.

Ivanhoe sold a 49.5% share interest in Kamoa Holding Limited (Kamoa Holding) to Zijin Mining and a 1% share interest in Kamoa Holding to privately owned Crystal River in December 2015. Kamoa Holding holds an 80% interest in the project. Since the conclusion of the Zijin transaction, each shareholder has been required to fund expenditures at Kamoa-Kakula in an amount equivalent to its proportionate shareholding interest. Ivanhoe and Zijin Mining each hold an indirect 39.6% interest in the Kamoa-Kakula Mining Complex, Crystal River holds an indirect 0.8% interest and the DRC government holds a direct 20% interest.

Kamoa-Kakula’s Phase 1 and Phase 2 concentrator plants at dusk.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_002full.jpg

Health and safety at Kamoa-Kakula

At the end of December 2021, Kamoa-Kakula reached 2,696,794 work hours free of a lost-time injury. One lost-time injury occurred in Q4 2021. The project continues to strive toward its workplace objective of zero harm to all employees and contractors.

Kamoa-Kakula has successfully focused on prevention, preparation, and mitigation in managing the risks associated with COVID-19. Large-scale testing, combined with focused preventative measures, ensured that positive cases were quickly identified, isolated, and treated, with cross contamination kept to a minimum. Kamoa-Kakula also continues to focus intensively on rolling out vaccinations across the workforce and local communities. Maintaining this high standard of risk management remains a daily focus, to prevent future cases. More than two thousand employees have at minimum received their first dose of the vaccine.

The Kamoa Hospital continues to treat COVID-19 patients when required, as construction progresses well for the expansion and upgrade of the primary healthcare wing. Kamoa-Kakula’s highly experienced doctors and nurses apply the latest medical treatments, supported by a world-leading emergency response and paramedic team.

As the pandemic evolves, the medical team at the Kamoa Hospital continues to review and update risk-mitigation protocols, while ensuring that new medical advances are investigated and applied to protect the health and safety of employees and community members.

The new Kamoa Hospital is a world-class medical facility featuring state-of-the-art equipment and highly-experienced doctors, nurses and paramedics.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_003full.jpg

John Botomwito, Kamoa Copper’s Superintendent of Health, in the ICU ward of the new hospital.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_004full.jpg

Kamoa-Kakula summary of operating and financial data

| Q4 2021 | Q3 2021 | |||||

| Ore tonnes milled (000’s tonnes) | 1,059 | 861 | ||||

| Copper ore grade processed (%) | 5.96% | 5.89% | ||||

| Copper recovery (%) | 86.40% | 83.40% | ||||

| Copper in concentrate produced (tonnes) | 54,481 | 41,545 | ||||

| Payable Copper sold (tonnes) | 53,165 | 41,490 | ||||

| Sales revenue ($’000) | 488,536 | 342,584 | ||||

| Cost of sales per pound ($ per lb) | 1.12 | 1.08 | ||||

| Cash cost (C1) ($ per lb) | 1.28 | 1.37 | ||||

| EBITDA ($’000) | 357,619 | 233,212 |

Prior to the start of commercial production on July 1, 2021, 9,858 tonnes of copper in concentrate was produced in Q2 2021, bringing the total tonnes produced for the year ending December 31, 2021, to 105,884.

C1 cash costs are prepared on a basis consistent with the industry standard definitions by Wood Mackenzie cost guidelines, but are not measures recognized under IFRS. In calculating the C1 cash cost, the costs are measured on the same basis as the company’s share of profit from the Kamoa Holding joint venture that is contained in the financial statements. C1 cash costs are used by management to evaluate operating performance and include all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to final port of destination, which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of delivered, finished metal. C1 cash costs exclude royalties and production taxes and non-routine charges as they are not direct production costs.

C1 cash cost per pound of payable copper produced can be further broken down as follows:

| Q4 2021 | Q3 2021 | ||||||

| Mining | ($ per lb) | 0.27 | 0.36 | ||||

| Processing | ($ per lb) | 0.17 | 0.16 | ||||

| Logistics charges (delivered to China) | ($ per lb) | 0.37 | 0.35 | ||||

| Treatment, refining and smelter charges | ($ per lb) | 0.24 | 0.21 | ||||

| General and administrative expenditure | ($ per lb) | 0.23 | 0.29 | ||||

| C1 cash cost per pound of payable copper produced | ($ per lb) | 1.28 | 1.37 |

All figures in the above tables are on a 100%-project basis. Metal reported in concentrate is prior to refining losses or deductions associated with smelter terms.

Copper concentrate production from the initial 3.8-Mtpa Kakula concentrator plant commenced in May 2021; commercial production achieved on July 1, 2021

First ore was introduced into the Phase 1, 3.8-Mtpa concentrator on May 20, 2021, and the first saleable concentrate was filtered on May 25, 2021, marking the start of concentrate production of the project’s Phase 1 concentrator plant and associated facilities.

The Kamoa-Kakula Mining Complex was deemed to have reached commercial production on July 1, 2021, after achieving a milling rate exceeding 80% of design capacity and recoveries close to 70% for a continuous, seven-day period. Revenue recognition, as well as depreciation of Kamoa-Kakula’s Phase 1 concentrator plant and milling operation, commenced on this date.

Copper recoveries progressively increased from an average of approximately 81% in July 2021 to approximately 85% in September 2021. Copper flotation recoveries averaged approximately 86% in Q4 2022 and achieved a record 88.5% in December 2021. The Phase 1, steady-state-design copper recovery is approximately 86%, depending on ore feed grade.

The Phase 1 concentrator currently is running at a throughput that is in excess of its design capacity of 3.8 Mtpa by more than 15%, with 117% of design throughput achieved in December.

54,481 tonnes of copper in concentrate were produced in Q4 2021, up from 41,545 in Q3 2021, for a total of 105,884 tonnes for the year ending December 31, 2021, for delivery to either the Lualaba Copper Smelter near Kolwezi, or to international markets.

Spot price of copper (US$/lb) over the last 12 months.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_005full.jpg

The Phase 2 high-pressure-grinding-rolls (HPGR) stockpile feed conveyor (on the right) began commissioning in February 2022. The Phase 1 HPGR feed conveyor and stockpile are on the left.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_006full.jpg

One of Kamoa-Kakula’s talented Congolese mining crews at the entrance to the Kakula Mine’s northern decline.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_007full.jpg

Project completion of Kamoa-Kakula’s Phase 2 processing plant almost complete; Phase 3 engineering studies and early works advancing well

Construction of Kamoa-Kakula’s Phase 2, 3.8-Mtpa concentrator plant almost is complete with early stage commissioning activities now underway. Hot commissioning of the concentrator with first ore and initial copper concentrate production are both on track for April 2022.

Engineering and early works for the Phase 3 expansion, including a new box cut and twin declines to access new mining areas, are progressing quickly. The third, significantly larger concentrator is being designed and is expected to be commissioned in Q4 2024. Phase 3 is expected to be fed from a combination of the established mine at Kansoko Sud, together with the new mines at Kamoa 1 and Kamoa 2. An updated pre-feasibility study, including the Phase 3 expansion, is expected in Q3 2022.

After successfully operating the Phase 1 concentrator for more than eight months, the Kamoa-Kakula team identified a number of relatively minor modifications that are expected to increase ore throughput from the current design of 475 tonnes per hour to 580 tonnes per hour. These modifications include increasing the diameter of a number of pipes, replacing a number of motors and pumps with larger ones and installing additional flotation, concentrate-thickening, concentrate-filtration and tailings-disposal capacity.

These modifications will allow the team to consistently operate the concentrator plant at the increased throughput without compromising plant availability, copper recovery or copper concentrate grade. Engineering design is underway and procurement of long-lead items already has started. This de-bottlenecking project is expected to cost approximately $50 million and will increase Kamoa-Kakula’s combined processing capacity to 9.2 Mtpa by Q2 2023.

Riaan Vermeulen, Kamoa Copper’s incoming Managing Director (middle-left) and Mark Farren, Kamoa Copper’s CEO (middle-right), with members of Zijin Mining’s senior management team during a recent Zijin site visit.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_008full.jpg

Members of Kamoa-Kakula’s diverse, multi-national team that has delivered the first two phases ahead of schedule, inside one of the new Phase 2 ball mills.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_009full.jpg

Excellent progress is being made on the excavation of Kamoa-Kakula’s new box cut that will provide access to the Kamoa 1 and Kamoa 2 mines, part of the project’s Phase 3 expansion.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_010full.jpg

Kamoa-Kakula smelter basic engineering underway

Early works on the planned direct-to-blister flash smelter at Kamoa-Kakula adjacent to the Phase 1 and Phase 2 concentrator plants is underway. The smelter is designed to use technology supplied by Outotec Oyj of Helsinki, Finland, and has been sized to process the bulk of the copper concentrate forecast to be produced by the Phase 1, 2 and 3 concentrator plants, with a production capacity of 500,000 tonnes per annum of blister copper.

China Nerin Engineering Company Co., Ltd. has been appointed to carry out the basic engineering design and develop a control budget estimate for the smelter; work is progressing well.

Ore stockpiles now hold more than 4.6 million tonnes grading 4.58% copper, containing more than 212,000 tonnes of copper at the end of February 2022

Kamoa-Kakula’s total high- and medium-grade ore surface stockpiles totalled approximately 4.65 million tonnes at an estimated grade of 4.58% copper as of the end of February 2022. The operation mined 1.70 million tonnes of ore grading 5.44% copper in Q4 2021, which was comprised of 1.52 million tonnes grading 5.60% copper from the Kakula Mine, including 0.81 million tonnes grading 6.68% copper from the mine’s high-grade centre, and 0.18 million tonnes grading 4.05% copper from the Kansoko Mine.

Kamoa-Kakula’s Phase 1 and Phase 2 concentrator plants and the ore stockpiles at the Kakula Mine’s northern decline. The direct-to-blister flash smelter is being constructed adjacent to the Phase 1 and Phase 2 concentrator plants.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_011full.jpg

Kamoa-Kakula delivering Phase 1 blister copper and copper concentrate under off-take agreements

Kamoa Copper’s off-take agreements are with CITIC Metal (HK) Limited (CITIC Metal) and Gold Mountains (H.K.) International Mining Company Limited, a subsidiary of Zijin, for 50% each of the copper products from Kamoa-Kakula’s Phase 1 production. The off-take agreements are evergreen for the production volumes from Phase 1, including copper concentrate and blister copper resulting from processing of copper concentrates at the nearby Lualaba Copper Smelter.

CITIC Metal and Zijin are purchasing the copper concentrate at the Kakula Mine and the blister copper at the Lualaba Copper Smelter on a free-carrier basis, meaning the buyers are responsible for arranging freight and shipment to the final destination, initially via the port of Durban, South Africa.

Kamoa-Kakula delivered its first bulk copper concentrates to the Lualaba Copper Smelter on June 1, 2021. The smelter is expected to treat up to 150,000 wet metric tonnes of copper concentrates from Kamoa-Kakula annually. Kamoa-Kakula began exporting its copper concentrate internationally in July 2021. The first truckloads of copper concentrate destined for smelters outside of the DRC departed from the mine site on July 17, 2021.

Mwadingusha hydropower plant fully operational and providing 78 MW of clean electricity for Kamoa-Kakula’s phases 1 and 2; focus now shifted to upgrading turbine 5 at the Inga II hydropower plant to provide power for expansions

All six new turbines at the Mwadingusha hydropower plant were synchronized to the national electrical grid in August 2021, with each generating unit producing approximately 13 megawatts (MW) of power, for a combined output of approximately 78 MW.

In August 2021, Kamoa-Kakula’s energy company signed an extension of the existing financing agreement with La Société Nationale d’Electricité (SNEL) to upgrade turbine 5 at the Inga II hydropower complex. Since June 2021, rehabilitation scoping works and technical visits have been conducted by Stucky Ltd. of Renens, Switzerland, and Voith Hydro of Heidenheim, Germany, a leading engineering group. Voith Hydro, the contractor for upgrading turbine 5, has successfully rehabilitated two turbine generators at the adjoining Inga I hydropower plant, a project that was financed by the World Bank.

Turbine 5 is expected to produce 162 MW of renewable hydropower, providing the Kamoa-Kakula Copper Complex and the planned, associated smelter with abundant, sustainable electricity for future expansions.

Kamoa-Kakula aiming to be first net-zero carbon emitter among top-tier copper mines by electrifying mining fleet with state-of-the-art equipment powered by electric batteries or hydrogen fuel cells

In May 2021, Ivanhoe Mines announced its pledge to achieve net-zero operational greenhouse gas emissions (Scope 1 and 2) at the industry-leading Kamoa-Kakula Copper Mine.

In support of the Paris Agreement on climate change, and in the spirit of the commitments at the April 2021 Leaders Summit on Climate by the Chinese and American governments to sharply cut emissions, Ivanhoe Mines has committed to working with its joint-venture partners and leading underground mining equipment manufacturers to ensure that Kamoa-Kakula becomes the first net-zero operational carbon emitter among the world’s top-tier copper producers.

Since the Kamoa-Kakula mines and concentrator plants are powered by clean, renewable hydro-generated electricity, the focus of the company’s net-zero commitment will be on electrifying the project’s mining fleet with new, state-of-the-art equipment powered by electric batteries or hydrogen fuel cells.

Kamoa-Kakula is working closely with its mining equipment suppliers to decrease the use of fossil fuels in its mining fleet, and evaluate the viability, safety and performance of new electric, hydrogen and hybrid technologies. The mine plans to introduce them into its mining fleet as soon as they become commercially available.

Empowering local communities through sustainable development

Ivanhoe Mines founded the Sustainable Livelihoods Program in 2010 to strengthen food security and farming capacity in the host communities near Kamoa-Kakula by establishing an agricultural demonstration garden to support local farmers.

Today, approximately 900 community farmers are benefiting from the Sustainable Livelihoods Program, producing high-quality food for their families and selling the surplus for additional income. The Sustainable Livelihoods Program, which commenced with maize and other vegetable production, now includes fruit, aquaculture, poultry and honey.

Farmer Omba Gertrude Muwana (left) and Benoit Mujinga, Kamoa Copper’s Sustainability Agronomist, at one of the community gardens and fish-farming operations near Kamoa-Kakula.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_012full.jpg

Construction of 100 new fishponds is complete, bringing the total number of fishponds to 138. The project will significantly contribute toward local entrepreneurship and enhanced regional food security. A group of community participants took part in, and graduated as facilitators for, an adult literacy training program.

Newly constructed fish ponds near Kamoa-Kakula.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_013full.jpg

Additional non-farming-related activities continued during Q4 2021 and include education programs, enterprise and supplier development programs, and the supply of fresh water to a number of local communities using solar-powered boreholes. The planned community borehole project was completed, with all 35 boreholes drilled using local contractors, providing approximately 12,000 community members with easy access to clean water.

Construction, landscaping and equipping of the Kaponda Primary School was completed, thereby achieving another milestone in the ambition to advance the objectives set out in the United Nations Sustainable Development Goals. Local community enterprise programs continued including brick-making and sewing, which are planned for project expansion in 2022, as well as landscaping and gardening, which may be reviewed for business efficiency and continued growth.

Construction of resettlement houses for the relocation program is continuing as planned. To date, 129 homes have been relocated, with five households remaining. The remaining families are scheduled for relocation upon completion of the construction of their new homes. Construction of the community church at Kaponda was completed and the new church was officially handed over to the community. The livelihood restoration program focused on the distribution of 758 chickens for all project-affected people, as well as three goats each to all 45 beneficiaries. Additional livelihood restoration efforts included planting of 3,600 orange seedlings to cover nine hectares, 1,000 grafted avocados across 10 hectares and approximately 54 hectares of cassava.

COPPER PRODUCTION GUIDANCE FOR 2022

The Kamoa-Kakula joint venture produced a total of 105,884 tonnes of copper in concentrate for the year ending December 31, 2021. The figures are on a 100%-project basis and metal reported in concentrate is prior to refining losses or deductions associated with smelter terms.

Guidance for 2022 is based on a number of assumptions and estimates as of December 31, 2021, including among other things, assumptions about the timing of the Phase 2 expansion and anticipated costs and expenditures. Production and cost guidance assumes the Phase 2 concentrator plant will commence copper production in Q2 2022 and that ramp-up will be in line with what was achieved with Phase 1. Guidance involves estimates of known and unknown risks, uncertainties and other factors which may cause the actual results to be materially different.

| Kamoa-Kakula 2022 Guidance | |||

| Contained copper in concentrate (tonnes) | 290,000 to 340,000 | ||

| Cash cost (C1) ($ per pound) | 1.20 to 1.40 |

Cash costs (C1) per pound of payable copper was $1.37/lb for Q3 2021 and was $1.28/lb for Q4 2021, reflecting the measured ramp-up of production at Kamoa-Kakula to steady state, and is expected to trend downward as the Phase 2 concentrator plant is commissioned and the mine’s fixed operating costs are spread over increased copper production.

C1 cash cost is a non-GAAP measure used by management to evaluate operating performance and includes all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to final port of destination (typically China), which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of delivered finished metal.

Cost of sales per pound of payable copper sold for Q4 2021 was $1.12/lb. For historical comparatives, see the Non-GAAP Financial Performance Measures section of this news release.

2. Platreef Project

64%-owned by Ivanhoe Mines

South Africa

The Platreef Project is owned by Ivanplats (Pty) Ltd (Ivanplats), which is 64%-owned by Ivanhoe Mines. A 26% interest is held by Ivanplats’ historically-disadvantaged, broad-based, black economic empowerment (B-BBEE) partners, which include 20 local host communities with approximately 150,000 people, project employees and local entrepreneurs. Ivanplats reached Level 4 contributor status in its most recent verification assessment on the B-BBEE scorecard. A Japanese consortium of ITOCHU Corporation, Japan Oil, Gas and Metals National Corporation, and Japan Gas Corporation, owns a 10% interest in Ivanplats, which it acquired in two tranches for a total investment of $290 million.

The Platreef Project hosts an underground deposit of thick, platinum-group metals, nickel, copper and gold mineralization on the Northern Limb of the Bushveld Igneous Complex in Limpopo Province – approximately 280 kilometres northeast of Johannesburg and eight kilometres from the town of Mokopane.

On the Northern Limb, platinum-group metals mineralization primarily is hosted within the Platreef, a mineralized sequence that is traced more than 30 kilometres along strike. Ivanhoe’s Platreef Project, within the Platreef’s southern sector, is comprised of two contiguous properties: Turfspruit and Macalacaskop. Turfspruit, the northernmost property, is contiguous with, and along strike from, Anglo Platinum’s Mogalakwena group of mining operations and properties.

Since 2007, Ivanhoe has focused its exploration and development activities on defining and advancing the down-dip extension of its original discovery at Platreef, now known as the Flatreef Deposit, which is amenable to highly-mechanized, underground mining methods. The Flatreef area lies entirely on the Turfspruit and Macalacaskop properties that form part of the company’s mining right.

Health and safety at Platreef

As at the end of December 2021, the Platreef Project reached a total of 677,450 lost-time, injury-free hours worked.

Kgalalelo Tladi, Chief Safety Officer, conducting a safety inspection of the Shaft 1 underground equipping stage.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_014full.jpg

COVID-19 protocols are continuously reviewed and optimized; as a result, the company implemented several measures to prevent and mitigate the escalation of infections. Those measures included the mass testing of employees and visitors, provision of transport to employees and a vaccination rollout.

By the end of December 2021, a total of 6,516 COVID-19 tests had been conducted. In support of the National Department of Health’s national vaccine rollout strategy, Ivanplats launched an on-site COVID-19 vaccination campaign that has administered 470 vaccine doses to date. Approximately 70% of the Platreef Project’s employees and contractors working on site have at minimum received their first dose of the vaccine.

Outstanding results of new Platreef feasibility study

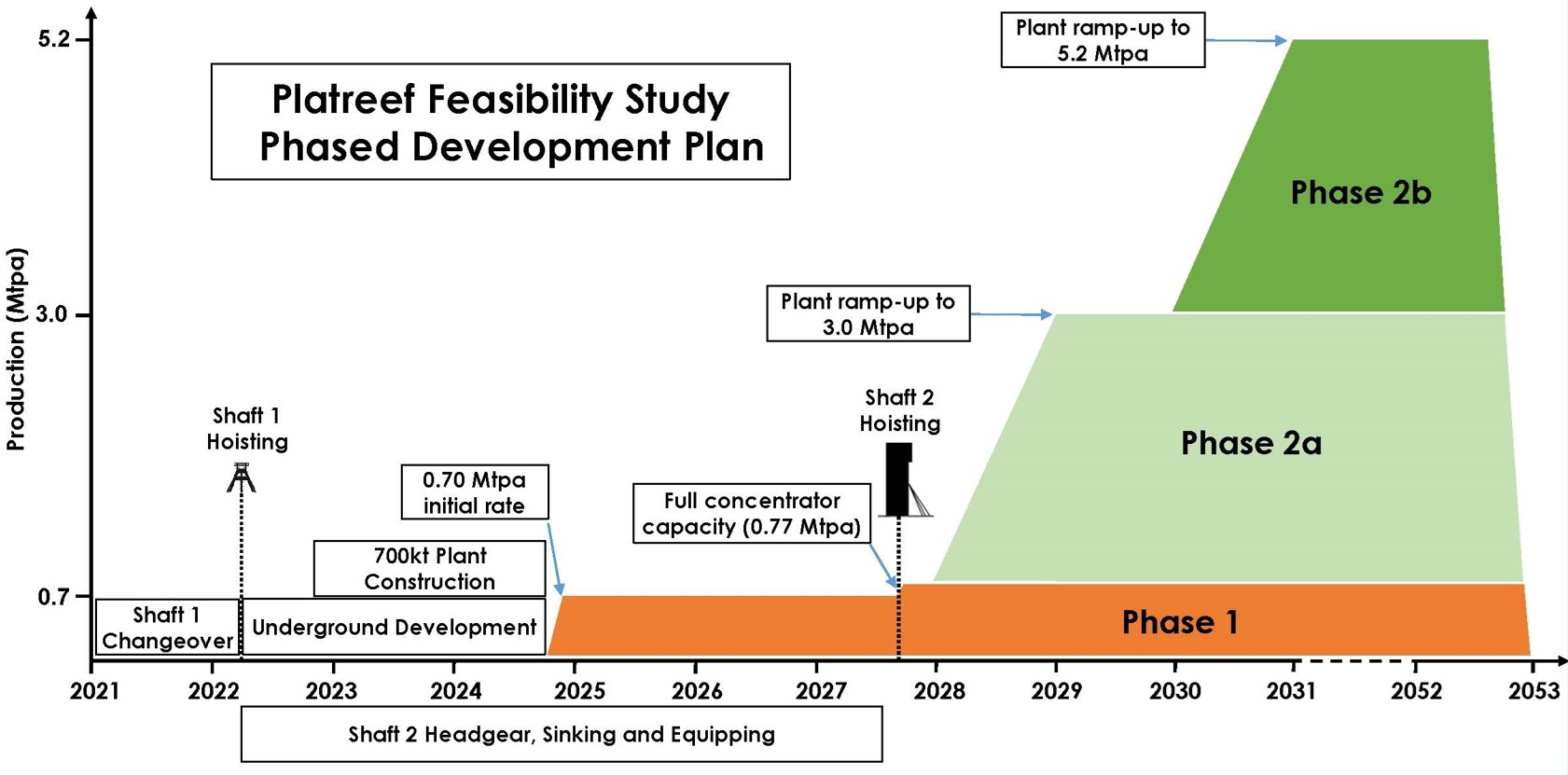

On February 28, 2022, Ivanhoe Mines announced the results of a new independent feasibility study for the Platreef Project (Platreef 2022 FS). The Platreef 2022 FS builds on the excellent results of the preliminary economic assessment (PEA) for an alternate scenario to expedite production, announced in November 2020, alongside the 2020 feasibility study.

The Platreef 2022 FS is based on a steady-state production rate of 5.2 Mtpa, as well as an accelerated ramp up to steady state through the earlier development of Shaft 2. The Platreef 2022 FS is based on the detailed design and engineering scenario first presented in the 2020 PEA, confirming the viability of a new phased-development pathway to fast-track Platreef into production by Q3 2024.

Highlights of the Platreef 2022 FS include:

- The Platreef 2022 FS evaluates the phased development of Platreef, with an initial 700-ktpa underground mine and a 770-ktpa capacity concentrator, targeting high-grade mining areas close to Shaft 1, with an initial capital cost of $488 million.

- First concentrate production for Phase 1 is planned for Q3 2024, with the Phase 2 expansion based on the commissioning of Shaft 2 in 2027, followed by the commissioning of two 2.2-Mtpa concentrators in 2028 and 2029. This would increase the steady-state production to 5.2 Mtpa by using Shaft 2 as the primary production shaft.

- Expansion capital cost for Phase 2 is estimated at $1.5 billion, which may be partially funded by cash flows from Phase 1 and a project financing package.

- Ivanplats’ dedicated engineering teams and leading consultants are evaluating optimizations to the sinking methodology for Shaft 2 to further accelerate the availability of the shaft for hoisting, which may accelerate the overall development timeline.

- Phase 1 average annual production of 113,000 ounces (oz.) of palladium, rhodium, platinum and gold (3PE+Au), plus 5 million pounds of nickel and 3 million pounds of copper.

- Phase 2 average annual production of 591,000 oz. of 3PE+Au, plus 26 million pounds of nickel and 16 million pounds of copper, which would rank Platreef as the fifth largest primary PGM producer on a palladium equivalent basis.

- Life-of-mine cash cost of $514 per ounce of 3PE+Au, net of by-products, and including sustaining capital costs, would rank Platreef as the industry’s lowest cost primary PGM producer.

- After-tax net present value at an 8% discount rate (NPV8%) of $1.7 billion and an internal rate of return (IRR) of 18.5%, based on long-term consensus prices.

- The sensitivity analysis at current metal prices of approximately $1,121/oz platinum, $2,979/oz palladium, $22,200/oz rhodium, $1,995/oz gold, $4.84/lb copper and $13.12/lb nickel (March 7, 2022), results in an after-tax NPV8% of $5.1 billion with an after-tax real IRR of 33%.

Figure 1: Production and timeline schematic of Platreef 2022 feasibility study.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_015full.jpg

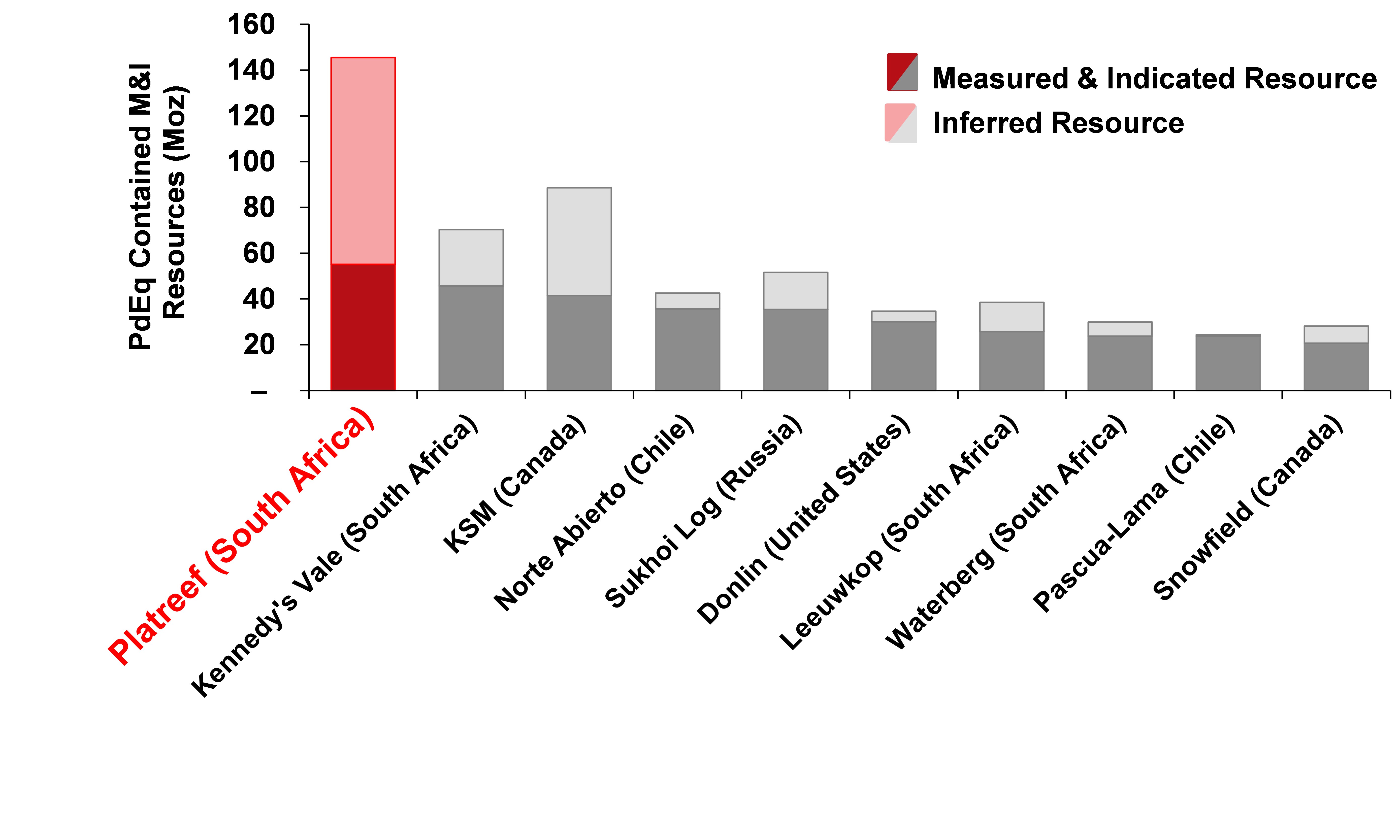

Figure 2: World’s largest precious metal deposits under development ranked by contained metal in Measured and Indicated Resources.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_016full.jpg

Source: Company filings, S&P Global Market Intelligence. Notes: Chart ranks the largest undeveloped primary palladium, platinum, gold, silver and rhodium projects from the S&P Global Market Intelligence database based on measured and indicated palladium equivalent resource. Palladium equivalent calculation includes palladium, platinum, gold, silver and rhodium ounces and has been calculated using spot price metal price assumptions (February 23, 2022) of $1,095/oz platinum, $2,480/oz palladium, $18,750/oz rhodium, $1,909/oz gold and $24.55/oz silver. Measured and Indicated resources for Platreef correspond to palladium, platinum, gold and rhodium ounces at a 1 g/t cut-off grade.

Platreef secures $200 million gold stream financing and additional $100 million palladium and platinum stream

In December 2021, Ivanplats entered into a gold, palladium and platinum stream financing with Orion Mine Finance, a leading international provider of customized financing to mining companies, and Nomad Royalty Company, a precious metals royalty company, in which Orion Mine Finance is a significant shareholder (Orion Mine Finance and Nomad Royalty Company, together, the Stream Purchasers). This transaction will fund a large portion of the Phase 1 capital costs, with first concentrate production for Phase 1 planned for Q3 2024.

The stream facilities are a prepaid forward sale of refined metals, with prepayments totalling $300 million, available in two tranches with the first prepayment of $75 million received in December 2021 following the closing of the transaction, and $225 million to be paid upon satisfaction of certain conditions precedent.

Under the terms of the $200 million gold stream agreement, the Stream Purchasers will receive an aggregate total of 80% of contained gold in concentrate until 350,000 ounces have been delivered, after which the stream will be reduced to 64% of contained gold in concentrate for the remaining life of the facility. The expected life of this facility will extend from the effective date of the stream agreement until the date when 685,280 ounces of gold have been delivered to the Stream Purchasers. The Stream Purchasers will purchase each ounce of gold at a price equal to the lower of the market price of gold or $100 per ounce.

Under the terms of the $100 million palladium and platinum stream agreement, Orion Mine Finance will receive an aggregate total of 4.2% of contained palladium and platinum in concentrate until 350,000 ounces have been delivered, after which the stream will be reduced to 2.4% for the remaining life of the facility. The expected life of this facility will extend from the effective date of the stream agreement until the date when 485,115 ounces of palladium and platinum have been delivered to the purchaser, which will pay for each ounce at a price equal to 30% of the market price of palladium and platinum.

Members of the Orion Mine Finance and Nomad Royalty teams, with members of Platreef’s mine development team, on the top platform of Platreef’s Shaft 1 headgear.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_017full.jpg

Conclusion of the stream agreements allows Ivanplats to focus efforts on finalizing the senior debt facility

Société Générale and Nedbank were appointed as mandated lead arrangers for the project debt facility in early 2021. Both the gold stream facility, and palladium and platinum stream facility, will be subordinated to any senior secured financing.

The senior debt facility is anticipated to be used only after the stream facilities are fully drawn. Ivanplats remains flexible to raise additional debt or equity at a later date, and has pre-agreed with the Stream Purchasers the inter-creditor arrangements for any future senior debt. While the stream facilities are guaranteed by Ivanplats and secured over the assets and Ivanhoe’s shares of Platreef, there is no recourse to Ivanhoe Mines.

Shaft 1 changeover to a production shaft nearing completion

The construction of the 996-metre-level station at the bottom of Shaft 1 was completed in July 2020. Shaft 1 initially will be used to access the orebody and is approximately 450 metres away from a high-grade area of Flatreef that is planned for bulk, mechanized mining. The three development stations that will provide initial, underground access to the high-grade orebody also have been completed on the 750-, 850- and 950-metre levels.

The auxiliary winder has been installed and commissioned. The headgear, both winders, equipping stage, conveyances and control systems comply with the highest current industry safety standards, with proven and tested safety and redundancy systems in place.

The changeover construction at Shaft 1 is progressing to plan and is on schedule to soon commence rock hoisting. All equipment for the shaft changeover has been procured and is on site. The changeover work within the shaft is being performed by Platreef’s experienced owners’ team.

Construction activities at the Platreef Project site, including Shaft 1 on the left, and the hitch-to-collar advancement for Shaft 2 on the right.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_018full.jpg

The winder that was used to successfully sink Shaft 1 has been converted to function as the main equipping conveyance during the shaft changeover, and will serve as the permanent rock, personnel and material winder following the shaft-equipping phase. The shaft will be equipped with two cages on top of two 12.5-tonne skips with hoisting capacity of 1 million tonnes per year, resulting from an amended configuration that does not require the cage to be interchanged mid-shift, thereby increasing the hoisting time during the initial phase of mining.

Shaft equipping commenced in May 2021 and remains on track to be completed by the end of March 2022. Following the completion of the changeover work in the shaft, underground stations, and establishment of the ore and waste passes, lateral underground mine development will commence toward high-grade ore zones.

Key electric underground mining equipment orders placed

Ivanplats placed an initial order with Epiroc of Stockholm, Sweden, for its primary mining fleet consisting of emissions-free, battery electric jumbo face drill rigs and load haul dump (LHD) vehicles, due for delivery in the next few months. The mine development contract was successfully concluded with Murray & Roberts Cementation, with site on-boarding well advanced, and the first blast on the 950-metre level anticipated in April 2022.

Shaft 2 headgear construction from hitch to collar well underway

Early works surface construction for Shaft 2 began in 2017, including the excavation of a surface box-cut to a depth of approximately 29 metres below surface and construction of the concrete hitch for the 103-metre-tall concrete headgear (headframe), which will house the shaft’s permanent hoisting facilities and support the shaft collar.

The Shaft 2 headframe construction, from the hitch to the collar level, is progressing well with the sixth and seventh headgear lifts completed and the eighth and final lift well advanced. Construction of the eight civil lifts, including a ventilation plenum and personnel access tunnel, is targeted for completion in May 2022.

Long-term supply of bulk water for the Platreef Mine

The water requirement for the Phase 1 operation is projected to peak at approximately three million litres per day, which will then increase to nine million litres per day once the Phase 2 expansion is complete. On January 17, 2022, Ivanhoe announced the signing of new agreements for the rights to receive local, treated water to supply the bulk water needed for the phased development plan at Platreef. These agreements replace those originally signed in 2018.

Under the terms of a new offtake agreement, the Mogalakwena Local Municipality (MLM) has agreed to supply at least three million litres per day of treated effluent, up to a maximum of 10 million litres per day for 32 years, from the date of first production, sourced from the town of Mokopane’s Masodi Waste Water Treatment Works, currently under construction.

Ivanplats also has signed a sponsorship agreement where Ivanplats has undertaken the commitment to complete the partially constructed Masodi Waste Water Treatment Works, which was halted in 2018. Ivanplats anticipates spending approximately ZAR 215 million ($14 million) to complete the works, whereby Ivanplats’ financial contribution will take the form of a sponsorship in favour of the municipality. Ivanplats will purchase the treated water at a reduced rate of ZAR 5 per thousand litres. Arrangements are underway to re-commence the construction works in Q3 2022, which are scheduled to take approximately 18 months.

Development of human resources and job skills

Implementation of the Platreef Project’s second Social and Labour Plan (SLP) is underway, through which Ivanplats plans to build on the first SLP and continue with its training and development suite, including 15 new mentors, internal skills training for 78 staff members, a legends program to prepare retiring employees with new/other skills, community adult education training for host community members, core technical skills training for at least 100 community members, portable skills training, and more.

The Platreef Project also continues to support several educational programs and the provision of free Wi-Fi in host communities. Community climate awareness was promoted through the implementation of a youth climate change action and tree-planting campaign at a local school.

Equipping of the mine’s permanent training academy is continuing, with the official launch being planned for later this year. Classrooms and offices at the training academy have been installed and the training and e-learning program has been instituted. A cadetship program, providing learnership opportunities to 49 local students was launched, offering a national certificate in health and safety, as well as mining competencies, such as utility vehicle operations from the Murray & Roberts Training Academy. The cadetship program seeks to enhance gender diversity, with 54% of the students being female.

Local economic development projects will contribute to community water-source development through the Mogalakwena Municipality boreholes program. Other projects, which will be conducted in partnership with other parties, include the refurbishment and equipping of a health clinic in Tshamahansi Village. In recognition of World Aids Day, a community health intervention to promote awareness and support, was implemented at the Tshamahansi clinic.

The enterprise and supplier development commitments comprise of expanding the existing kiosk and laundry facilities and adding expanded change house facilities to be managed by a community partner in the future. A five-year integrated business accelerator and funding project assists community members to obtain help with development and supplier readiness.

Spot price of palladium (US$/oz) over the past 12 months.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_019full.jpg

Spot price of rhodium (US$/oz) over the past 12 months.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_020full.jpg

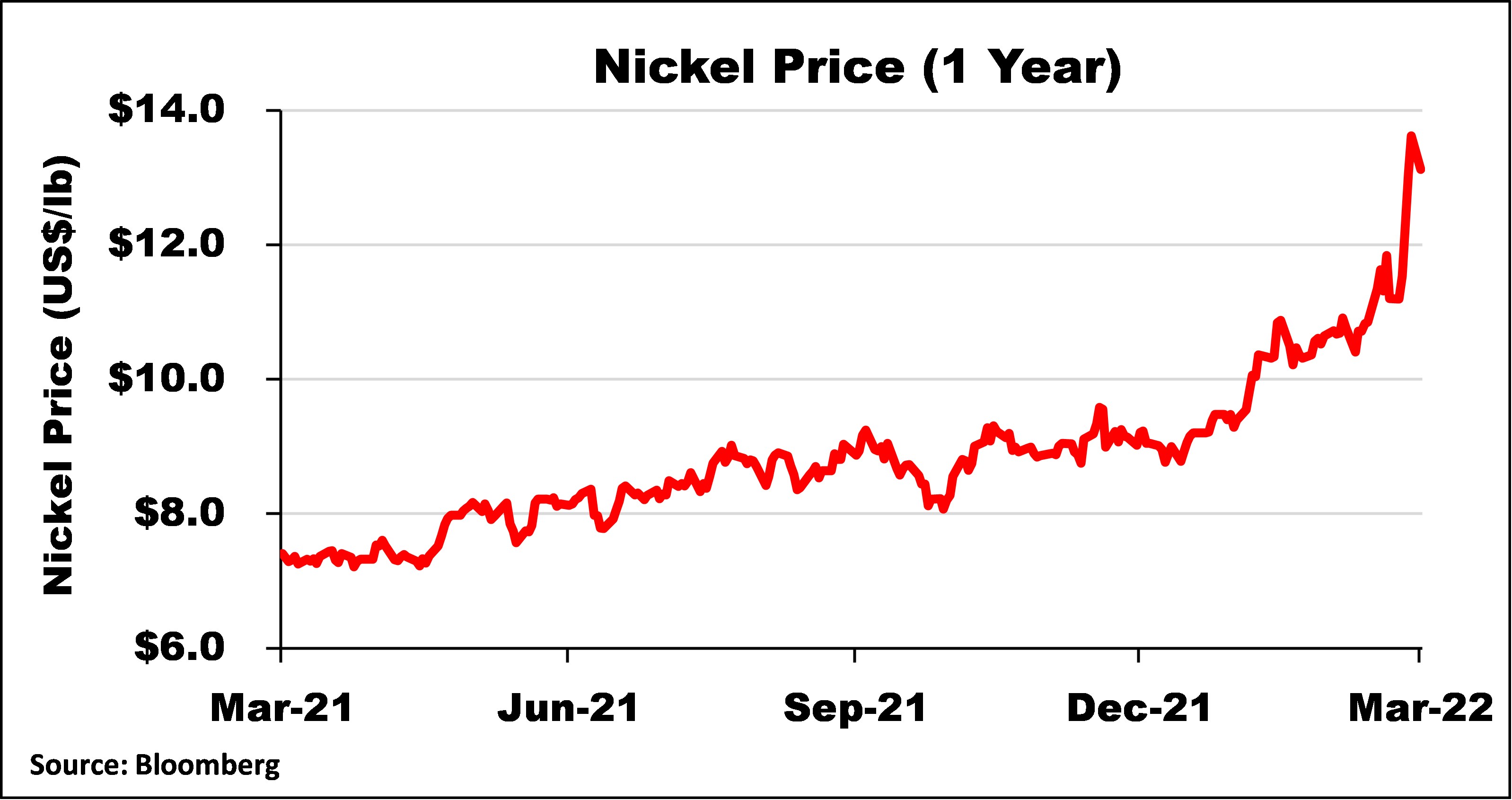

Spot price of nickel (US$/lb) over the past 12 months.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_021full.jpg

Spot price of platinum (US$/oz) over the past 12 months.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_022full.jpg

Spot price of gold (US$/oz) over the past 12 months.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_023full.jpg

3. Kipushi Project

68%-owned by Ivanhoe Mines

Democratic Republic of Congo

The Kipushi copper-zinc-germanium-silver-lead mine in the DRC is adjacent to the town of Kipushi and approximately 30 kilometres southwest of Lubumbashi. It is located on the Central African Copperbelt, approximately 250 kilometres southeast of the Kamoa-Kakula Mining Complex and less than one kilometre from the Zambian border.

Ivanhoe acquired its 68% interest in the Kipushi Project in November 2011, through Kipushi Holding that is 100%-owned by Ivanhoe Mines. The balance of 32% in the Kipushi Project is held by the state-owned mining company, Gécamines.

Kipushi Holding and Gécamines have signed a new agreement to return the ultra-high-grade Kipushi Mine back to commercial production. Kipushi will be the world’s highest-grade major zinc mine, with an average grade of 36.4% zinc over the first five years of production.

(L-R) Olivier Binyingo (Ivanhoe Mines Vice President, Public Affairs DRC), Marna Cloete (Ivanhoe Mines President), Alphonse Kaputo Kalubi (Chairman of Gécamines), and Louis Watum (General Manager, Kipushi Corporation) discussing the Kipushi partnership during a recent visit to the Kamoa-Kakula mining complex.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_024full.jpg

The new agreement sets out the commercial terms that will form the basis of a new Kipushi joint-venture agreement, establishing a robust framework for the mutually beneficial operation of the Kipushi Mine for years to come, and is subject to execution of definitive documentation.

Highlights of the new agreement include:

-

Kipushi Holding will transfer 6% of the share capital and voting rights in the Kipushi Project to Gécamines, after which Kipushi Holding and Gécamines will hold 62% and 38%, respectively.

-

From January 25, 2027, 5% of the share capital and voting rights in the Kipushi Project shall be transferred from Kipushi Holding to Gécamines, after which Kipushi Holding and Gécamines will hold 57% and 43%, respectively.

-

In the event that, after the 6% and 5% transfers, part of the Kipushi Project’s share capital is required to be transferred to the State or to any third party pursuant to an applicable legal or regulatory provision, Gécamines shall transfer the number of the Kipushi Project shares required, and Kipushi Holding shall retain 57% ownership in the Kipushi Project.

-

Once a minimum of the current proven and probable reserves and up to 12 million tonnes has been mined and processed, an additional 37% of the share capital and voting rights in the Kipushi Project shall be transferred from Kipushi Holding to Gécamines, after which Kipushi Holding and Gécamines will hold 20% and 80%, respectively.

-

A new supervisory board and executive committee will be established with appropriate shareholder representation.

-

New initiatives will be implemented, focusing on the development of Congolese employees, including individual development, the identification of future leaders, succession planning and the promotion of gender equality across the workforce.

-

A framework for tendering for the offtake of zinc concentrates produced by the Kipushi Mine has been established, which includes Gécamines’ participation.

-

Kipushi Holding will continue to fund the Kipushi Project with the shareholder loan and/or procure financing from third parties for the development of the project. The interest on the shareholder loan will be 6%, which will be applicable from January 1, 2022, on the existing balance and any further advances. Under the terms of the current shareholder loan agreement, the shareholder loan carries interest of LIBOR plus 4%, which is applicable to 80% of the advanced amounts with the remaining 20% interest-free. As of December 31, 2021, the balance of the shareholder loan owing to Kipushi Holding, including accrued interest, was approximately $528 million.

Health and safety at Kipushi

At the end of December 2021, the Kipushi Project reached a total of 3,983,319 work hours free of lost-time injuries. It has been more than two and a half years since the last lost-time injury occurred at the project.

Since temporarily suspending mine development operations due to the COVID-19 pandemic, the project maintained a reduced workforce to safely and cost-effectively maintain infrastructure and pumping systems and to execute planned projects.

The Kipushi Project has built a new potable water station to provide a free daily supply of water to the municipality of Kipushi. This daily supply to the Kipushi municipality community members includes power supply, disinfectant chemicals, routine maintenance, security and emergency repair of leaks to the primary reticulation to the benefit of an estimated 100,000 people, excluding those from rural areas. Approximately 1,000 cubic metres of potable water is pumped hourly and continuously to consumers on a daily basis.

50 boreholes of potable water are planned to be drilled around the Kipushi district over five years, to reach areas not served by current distribution. To date, 12 solar-powered potable water wells have been drilled and currently are operating throughout the district.

The Kipushi Project continues to support educational initiatives through renovations at the Mungoti School, and the granting of bursaries and scholarships to students from Kipushi. Over the past year, approximately 100 students have been supported through the bursary program. The sewing training centre project established by the Kipushi Project continued producing cloth face masks, donating approximately 2,000 masks a month to host communities. The Kipushi Project also is broadcasting daily COVID-19 awareness messages on a local community radio station, as well as through a motorized caravan.

The pilot of the Sustainable Livelihoods Program, which commenced in 2020 with a poultry farming initiative established for the benefit of a consortium of local women, continued successfully, with plans for expansion around the Kipushi district in 2022. An annual tree-planting initiative was implemented to raise awareness and make a positive impact in respect of climate change mitigation.

Kipushi feasibility study issued, heralding the planned re-start of the historic mine, with a two-year development timeline and exceptional economic results

On February 14, 2022, Ivanhoe Mines announced the positive findings of an independent, feasibility study for the planned resumption of commercial production at Kipushi.

The Kipushi 2022 feasibility study builds on the results of the pre-feasibility study published by Ivanhoe Mines in January 2018. The redevelopment of Kipushi is based on a two-year construction timeline, which utilizes the significant existing surface and underground infrastructure to allow for substantially lower capital costs than comparable development projects. The estimated pre-production capital cost, including contingency, is $382 million.

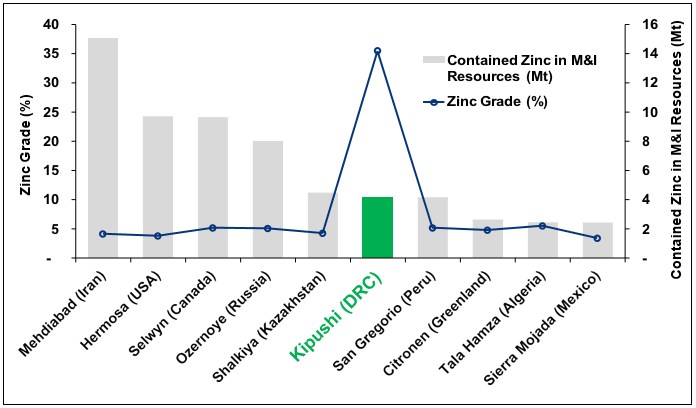

The 2022 feasibility study focuses on the mining of Kipushi’s zinc-rich Big Zinc and Southern Zinc zones, with an estimated 11.8 million tonnes of Measured and Indicated Mineral Resources grading 35.3% zinc. Kipushi’s exceptional zinc grade is more than twice that of the world’s next-highest-grade zinc project, according to Wood Mackenzie, a leading, international industry research and consulting group (see Figure 3).

Figure 3: World’s top 10 zinc projects, by contained zinc.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_025full.jpg

Source: Wood Mackenzie, January 2022. Note: All tonnes and metal grades of individual metals used in the equivalency calculation of the above-mentioned projects (except for Kipushi) are based on public disclosure and have been compiled by Wood Mackenzie. All metal grades have been converted by Wood Mackenzie to a zinc equivalent grade at Wood Mackenzie’s respective long-term price assumptions.

The 2022 feasibility study envisages the recommencement of underground mining operations, and the construction of a new concentrator facility on surface with annual processing capacity of 800,000 tonnes of ore, producing on average 240,000 tonnes of zinc contained in concentrate.

Highlights of the 2022 feasibility study results for the Kipushi Mine include:

-

The 2022 feasibility study evaluates the development of an 800-ktpa underground mine and concentrator, with an increased resource base compared to the pre-feasibility study, extending the mine life to 14 years.

-

Existing surface and underground infrastructure allows for significantly lower capital costs than comparable development projects, with the principal development activity being the construction of a conventional concentrator facility and new supporting infrastructure on surface in a two-year timeline.

-

Pre-production capital costs, including contingency, estimated at $382 million.

-

Life-of-mine average zinc production of 240,000 tonnes per annum, with a zinc grade of 32%, is expected to rank Kipushi among the world’s major zinc mines (Figure 3), once in production, with the highest grade by some margin.

-

Life-of-mine average C1 cash cost of $0.65/lb of zinc is expected to rank Kipushi, once in production, in the second quartile of the cash cost curve for zinc producers globally.

-

At a long-term zinc price of $1.20/lb, the after-tax net present value (NPV) at an 8% real discount rate is $941 million, with an after-tax real internal rate of return (IRR) of 40.9% and project payback period of 2.3 years.

-

The sensitivity analysis at current zinc prices of approximately $1.84/lb (March 7, 2022), results in an after-tax NPV8% of $3.0 billion with an after-tax real IRR of 86%.

The Kipushi 2022 feasibility study was independently prepared on a 100%-project basis by OreWin Pty. Ltd., MSA Group (Pty.) Ltd., SRK Consulting (Pty) Ltd. and METC Engineering.

Project development and infrastructure

Although development and rehabilitation activities in 2021, as well as in 2020, were limited, significant progress has been made in recent years to modernize the Kipushi Mine’s underground infrastructure as part of preparations for the mine to resume commercial production, including upgrading a series of vertical mine shafts to various depths, with associated headframes, as well as underground mine excavations and infrastructure.

A series of crosscuts and ventilation infrastructure still is in working condition and has been cleared of old materials and equipment to facilitate modern, mechanized mining. The underground infrastructure also includes a series of high-capacity pumps to manage the mine’s water levels, which now are easily maintained at the bottom of the mine.

Shaft 5 is eight metres in diameter and 1,240 metres deep and has been upgraded and re-commissioned. The main personnel and material winder has been upgraded and modernized to meet international industry standards and safety criteria. The Shaft 5 rock-hoisting winder also is fully operational, with new rock skips, new head- and tail-ropes, and attachments installed. The two newly manufactured rock conveyances (skips) and the supporting frames (bridles) have been installed in the shaft to facilitate the hoisting of rock from the main ore and waste storage silos feeding rock on the 1,200-metre level.

Since temporarily suspending mine development operations, priority engineering tasks still continued, including new winder installations as a second means of egress on the cascade side, and repairs, as well as replacement of main critical pump columns in Shaft 5 to ensure reliable and continued pumping of water from the mine.

Patrick Mwanza Wa Kabongo operating the modern, new hoist at Kipushi’s main production shaft (Shaft 5).

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_026full.jpg

Spot price of zinc (US$/lb) over the past 12 months.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_027full.jpg

Recently upgraded underground mine with easy access to stopes allows for rapid production ramp-up

Mining at Kipushi historically has been carried out from the surface to a depth of approximately 1,220 metres. Shaft 5 (P5) is planned to be the main production shaft with a maximum hoisting capacity of 1.8 Mtpa and provides the primary access to the lower levels of the mine, including the Big Zinc Zone, through the 1,150-metre haulage level.

Mining will be performed using highly productive, mechanized methods and cemented rock fill will be utilized to fill open stopes. Material generated underground will be trucked to the base of the P5 shaft, crushed and hoisted to surface. Personnel and equipment access also are via the P5 shaft. The Big Zinc Zone will be accessed via the existing decline, without significant new development required. As the existing decline already is below the first planned stoping level, it is relatively quick to develop the first zinc stopes for the ramp up of mine production.

Figure 4: Schematic section of Kipushi Mine. Shaft 5 (P5) is planned to be the main production shaft with a maximum hoisting capacity of 1.8 Mtpa.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_028full.jpg

4. Western Foreland Exploration Project

90%- and 100%-owned by Ivanhoe Mines

Democratic Republic of Congo

Ivanhoe’s DRC exploration group is targeting Kamoa-Kakula-style copper mineralization through a regional exploration and drilling program on its Western Foreland exploration licences, located to the north, south and west of the Kamoa-Kakula Mining Complex. Ivanhoe’s Western Foreland Exploration Project consists of 17 licences that cover a combined area of approximately 2,550 square kilometres.

Exploration models that successfully led to the discoveries of Kakula, Kakula West, and the Kamoa North Bonanza Zone on the Kamoa-Kakula joint-venture mining licence are being applied to the extensive Western Foreland land package by the same team of exploration geologists responsible for the previous discoveries.

Exploration drilling in Q4 2021 was focused on wide-scale regional dip sections along the axis of the Western Foreland permits at approximately 10km intervals. The drilling was designed to provide detailed stratigraphic and structural information ahead of processing and interpreting the geophysical surveys. The drill holes currently are being surveyed with downhole geophysical tools to provide density, conductivity and velocity information.

Surface soil and stream-sediment sampling focused on the southwest permits. 18 stream samples and 462 soil samples were collected during Q4 2021. The mapping of the southwest permits continued, with interpretation ongoing.

Construction of the access spine road across the western permits now has reached a total length of 69 kilometres. Container-based bridges were installed along the entire length of the road to provide all season access to the full extent of the southwest foreland. Some additional wet season access roads were completed to allow additional drilling during the wet season.

Geophysical airborne surveys such as magnetics, gravity and electromagnetics recommenced in Q4 2021. This new geophysical data will enhance the target delineation program for drill testing and soil sampling, as well as provide a better understanding of the structural domains of the area. Magnetics and gravity were completed by the end of the year with the electromagnetic survey and additional gravity survey 46% completed by the end of the year. Ground gravity survey work commenced during Q4 2021 and will be used in conjunction with the airborne gravity to provide increased definition where required.

Ivanhoe’s 2022 Western Foreland exploration expenditure is provisionally planned at $25 million. The main component of this expenditure is exploration drilling, with more than 50,000 metres of shallow (depth of less than 150 metres), air core, reverse circulation and diamond drilling focussed on defining sub-outcrop positions and obtaining bed-rock samples under the Kalahari sand cover. In addition, up to 45,000 metres of deeper regional drilling covering the entire 2,550-square-kilometre land package also is provisionally planned, some of which is dependent upon exploration success.

South Africa-based New Resolution Geophysics conducting an airborne electro-magnetic survey over Ivanhoe’s Western Foreland exploration licences in February 2022. The electro-magnetic survey is the last of three geophysical surveys to be completed over the Western Foreland licences, providing geologists with ultra-high resolution data for the 2022 drilling campaign.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_030full.jpg

SELECTED ANNUAL FINANCIAL INFORMATION

This selected financial information is in accordance with IFRS as presented in the annual consolidated financial statements. Ivanhoe had no operating revenue in any financial reporting period. All operating revenue from commercial production at the Kamoa-Kakula Mining Complex is recognized within the Kamoa Holding joint venture. Ivanhoe did not declare or pay any dividend or distribution in any financial reporting period.

Table 1

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_031full.jpg

DISCUSSION OF RESULTS OF OPERATIONS

Review of the year ended December 31, 2021 vs. December 31, 2020

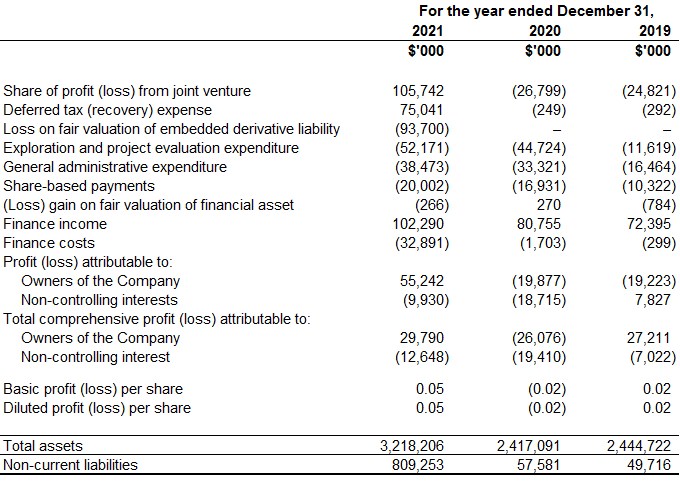

The company recorded total comprehensive income of $17.1 million for the year ended December 31, 2021, compared to a total comprehensive loss of $45.5 million for the year ended December 31, 2020. The main contributor to the profit for 2021 was the company’s share of the profit from the Kamoa Holding joint venture.

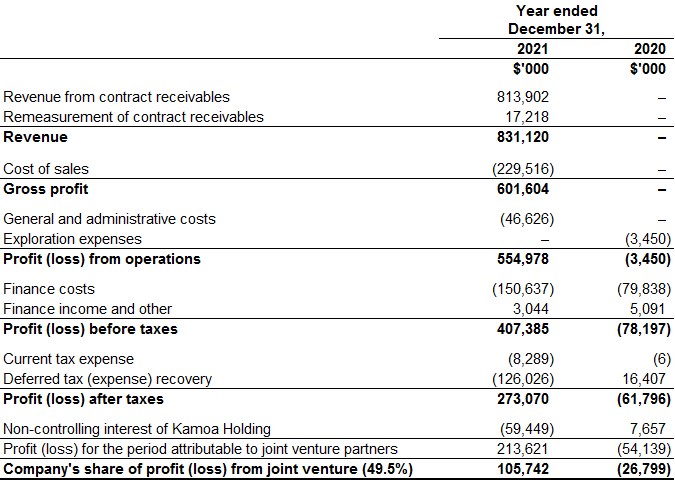

The Kamoa-Kakula Mining Complex reached commercial production on July 1, 2021 and sold 94,655 tonnes of payable copper in 2021 realizing revenue of $831.1 million for the Kamoa Holding joint venture. The company recognized income in aggregate of $199.6 million from the joint venture in 2021, which can be summarized as follows:

Table 2

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_032full.jpg

The company’s share of profit from the Kamoa Holding joint venture was $105.7 million for the year ended December 31, 2021, compared to a loss of $26.8 million for the same period in 2020, the breakdown of which is summarized in the following table:

Table 3

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_033full.jpg

Of the $150.6 million finance costs recognized in the Kamoa Holding joint venture for 2021, $133.8 million (2020: $79.8 million) relates to shareholder loans where each shareholder is required to fund Kamoa Holding in an amount equivalent to its proportionate shareholding interest. Of the remaining finance costs, $13.5 million relates to the $300 million advance payment facility and provisional payment facility available under Kamoa-Kakula’s offtake agreements, while $3.3 million relates to the equipment financing facilities.

Exploration and project evaluation expenditure amounted to $52.2 million for the year ended December 31, 2021 and was $7.5 million more than for the same period in 2020 ($44.7 million). Exploration and project evaluation expenditure related to exploration at Ivanhoe’s Western Foreland exploration licences and amounts spent at the Kipushi Project which was on reduced activities and incurred limited cost of a capital nature during 2021 and 2020.

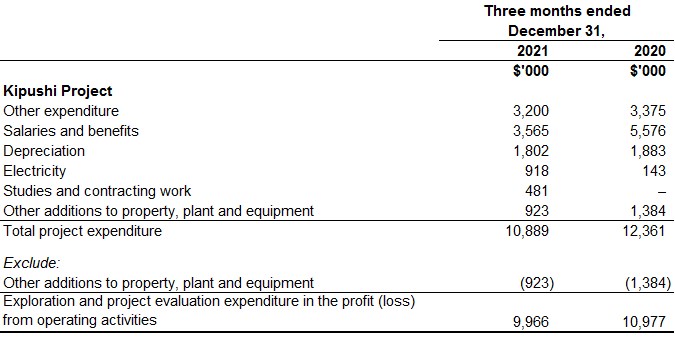

The main classes of expenditure at the Kipushi Project for the year ended December 31, 2021, and for the same period in 2020 are set out in the following table:

Table 4

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_034full.jpg

Finance income amounted to $102.3 million for the year ended December 31, 2021, and $80.8 million for the same period in 2020. Included in finance income is the interest earned on loans to the Kamoa Holding joint venture to fund operations that amounted to $93.9 million for 2021, and $70.4 million for 2020. Interest increased as the accumulated loan balance increased.

The company recognized a loss on fair valuation of the embedded derivative financial liability of $93.7 million for 2021.

With the completion of the stream financing facilities in December 2021, which will fund a large portion of the Platreef Project’s Phase 1 capital costs, and supported by the excellent results of the Platreef 2022 FS, it is now deemed probable that future taxable profit will be available from the Platreef Project, against which the unused tax losses and unused tax credits can be utilized. As a result, the company recognized the previously unrecognized deferred tax asset in December 2021, resulting in a deferred tax recovery (income) of $75.0 million.

The total comprehensive income for 2021, included an exchange loss on translation of foreign operations of $28.2 million, resulting from the weakening of the South African Rand by 9% from December 31, 2020, to December 31, 2021, compared to an exchange loss on translation of foreign operations recognized for the same period in 2020 of $6.9 million.

Financial position as at December 31, 2021 vs. December 31, 2020

The company’s total assets increased by $801.1 million, from $2,417.1 million as at December 31, 2020, to $3,218.2 million as at December 31, 2021. The main reason for the increase in total assets was the receipt of the net proceeds from the convertible senior notes that closed on March 17, 2021. The net proceeds from the convertible notes, after deducting the expenses of the offering that related to the host liability of $10.5 million, was $564.5 million.

Cash and cash equivalents increased by $345.4 million, from $262.8 million as at December 31, 2020, to $608.2 million as at December 31, 2021 due to the receipt of the convertible note proceeds, as well as the first draw down of the stream facilities in aggregate of $75 million. The company utilized $7.1 million of its cash resources in its operations and advanced loans of $152.7 million to the Kamoa Holding joint venture during the twelve months ended December 31, 2021.

The company’s total liabilities increased by $760.6 million to $841.2 million as at December 31, 2021, from $80.6 million as at December 31, 2020, with the increase mainly due to the private placement offering of $575.0 million of 2.50% convertible senior notes described in the company’s 2021 Year-End MD&A, as well as the deferred revenue recognized on the stream facility of $69.6 million after transaction costs. The deferred revenue represents the prepayment for the future sale of refined gold and palladium and platinum to be delivered by the Platreef Project in the future and will be amortized as ounces are delivered to the Stream Purchasers.

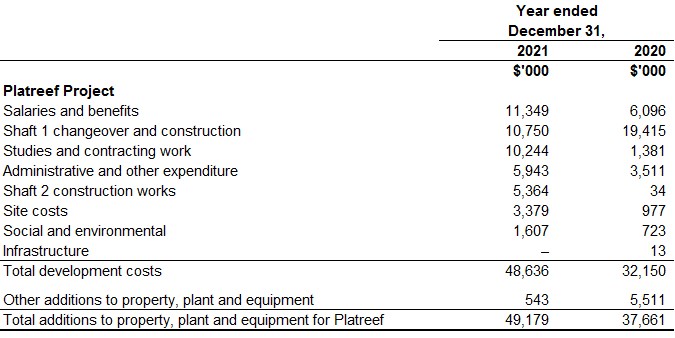

The net increase in property, plant and equipment amounted to $17.6 million, with additions of $52.7 million to project development and other property, plant and equipment. Of this total, $49.2 million pertained to development costs and other acquisitions of property, plant and equipment at the Platreef Project.

The main components of the additions to property, plant and equipment – including capitalized development costs – at the Platreef Project for the year ended December 31, 2021, and for the same period in 2020, are set out in the following table:

Table 5

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_035full.jpg

Costs incurred at the Platreef Project are deemed necessary to bring the project to commercial production and are therefore capitalized as property, plant and equipment.

The company’s investment in the Kamoa Holding joint venture increased by $352.3 million from $1,289.5 million as at December 31, 2020, to $1,641.8 million as at December 31, 2021. The company’s portion of the Kamoa Holding joint venture cash calls amounted to $152.7 million for the year ended December 31, 2021, while the company’s share of profit from the joint venture amounted to $105.7 million.

The company’s investment in the Kamoa Holding joint venture can be broken down as follows:

Table 6

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_036full.jpg

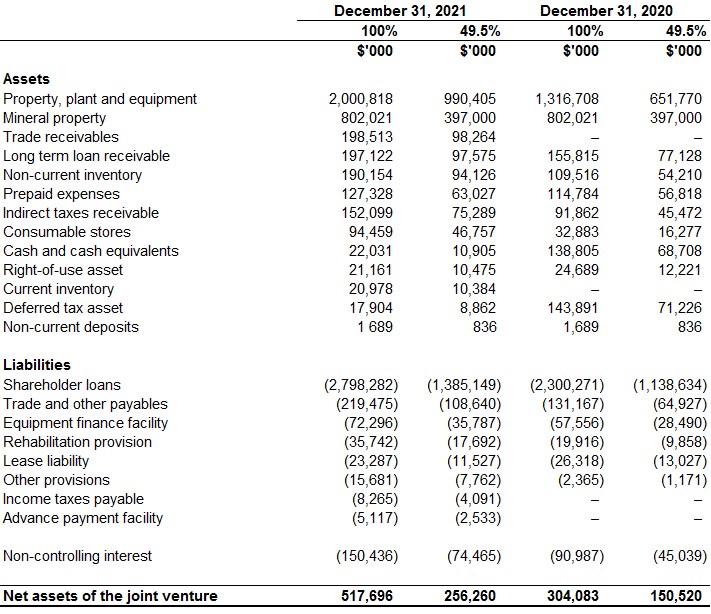

Prior to commencing commercial production in July 2021, the Kamoa Holding joint venture principally used loans advanced to it by its shareholders to advance the Kamoa-Kakula Project through investing in development costs and other property, plant and equipment. This can be evidenced by the movement in the company’s share of net assets in the Kamoa Holding joint venture which can be broken down as follows:

Table 7

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_037full.jpg

Going forward, all Phase 1 operating costs and the majority of Phase 2 and Phase 3 capital expenditures are expected to be funded from copper sales and facilities in place at Kamoa-Kakula. Cash generated in excess of operational and expansion requirements is expected to be utilized to commence shareholder loan repayments. Based on current market conditions, it is anticipated that shareholder loan repayments from Kamoa-Kakula will commence in 2022.

The Kamoa Holding joint venture completed the draw-down of EUR 45 million (approximately $56 million) of the equipment financing and $9 million of the down-payment facilities in late December 2020. Additional drawdowns on the equipment financing of EUR 22.7 million were made in 2021 bringing the total amount drawn to EUR 67.2 million (approximately $76.1 million) at December 31, 2021. The equipment finance is secured only by the equipment that is being financed and has an effective interest rate of 8.96%. The down-payment facility is unsecured and has an effective interest rate of 11.58%.

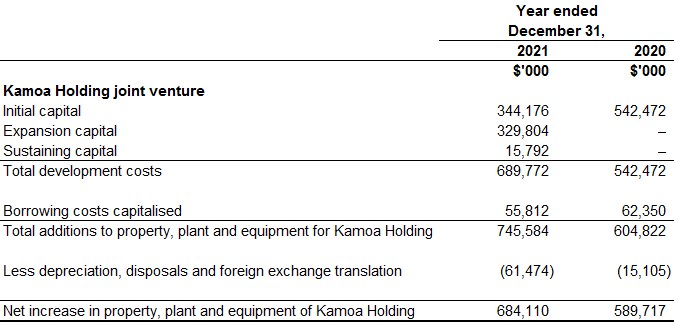

The Kamoa Holding joint venture’s net increase in property, plant and equipment from December 31, 2020, to December 31, 2021, amounted to $684.1 million and can be further broken down as follows:

Table 8

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_038full.jpg

SELECTED QUARTERLY FINANCIAL INFORMATION

The following table summarizes selected financial information for the prior eight quarters. Ivanhoe had no operating revenue in any financial reporting period. All revenue from commercial production at the Kamoa-Kakula Mining Complex is recognized within the Kamoa Holding joint venture. Ivanhoe did not declare or pay any dividend or distribution in any financial reporting period.

Table 9

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_039full.jpg

Review of the three months ended December 31, 2021 vs. December 31, 2020

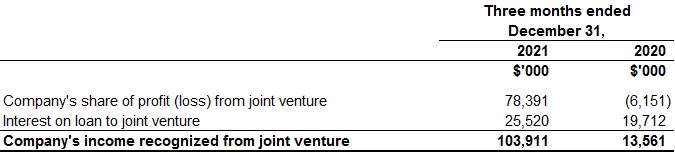

The company recorded a profit for Q4 2021 of $48.2 million compared to a loss of $10.9 million for the same period in 2020, with the company’s share of the profit from the Kamoa Holding joint venture being a key contributor to the Q4 2021 profit. The total comprehensive income for Q4 2021 was $30.4 million compared to $31.8 million for Q4 2020.

The Kamoa-Kakula Mining Complex sold 53,165 tonnes of payable copper in Q4 2021 realizing revenue of $488.5 million for the Kamoa Holding joint venture. The company recognized income in aggregate of $103.9 million from the joint venture in Q4 2021, which can be summarized as follows:

Table 10

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_040full.jpg

The company’s share of profit from the Kamoa Holding joint venture was $78.4 million in Q4 2021 compared to a loss of $6.2 million in Q4 2020. The following table summarizes the company’s share of profit (loss) of the joint venture for the three months ended December 31, 2021, and for the same period in 2020:

Table 11

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115940_ef5f0968941bd85e_041full.jpg

Of the $55.6 million finance costs recognized in the Kamoa Holding joint venture for Q4 2021, $45.7 million (Q4 2020: $21.3 million) relates to shareholder loans where each shareholder funded Kamoa Holding in an amount equivalent to its proportionate shareholding interest. Of the remaining finance costs, $8.0 million relates to the $300 million advance payment facility and the provisional payment facility available under Kamoa’s offtake agreements and $1.8 million relates to the equipment financing facilities.

The company recognized a loss on fair valuation of the embedded derivative financial liability of $88.5 million for Q4 2021. Finance cost increased from $1.5 million for Q4 2020 to $10.5 million for the same period in 2021, $10.2 million of which related to the interest on the convertible notes at the effective interest rate.

With the completion of the stream financing facilities in December 2021, which will fund a large portion of the Platreef Project’s Phase 1 capital costs, and supported by the excellent results of the Platreef 2022 FS, it is now deemed probable that future taxable profit will be available from the Platreef Project, against which the unused tax losses and unused tax credits can be utilised. As a result, the company recognized the previously unrecognized deferred tax asset in Q4 2021, resulting in a deferred tax recovery (income) of $75.0 million in the period.

Finance income for Q4 2021 amounted to $28.0 million and was $7.0 million more than for the same period in 2020 ($21.0 million). Included in finance income is the interest earned on loans to the Kamoa Holding joint venture to fund operations that amounted to $25.5 million for Q4 2021, and $19.7 million for the same period in 2020, and increased as the accumulated loan balance increased.