The merger between

BHP Group

‘s

BHP

petroleum arm and Woodside Petroleum Ltd (Woodside) has been approved by Australia’s competition regulator, per a Reuters report. This clearance marks an important step toward the completion of the $28 billion merger, which will create a global top 10 independent oil and gas producer.

Given that the merger would combine two of the four largest domestic natural gas suppliers in Western Australia, it necessitated a close review on whether any competition concerns might emerge. After assessing the supply of domestic natural gas in Western Australia, ACCC announced that the merger will not reduce competition in the domestic gas market. It is worth mentioning that Woodside will have a 20% share in the market. It is expected to encounter adequate competition from a range of suppliers of domestic gas — both big and small.

BHP had announced the merger of its Petroleum business with Woodside on Aug 17. In November, BHP and Woodside signed a binding share sale agreement to merge their respective oil and gas portfolios. Woodside will acquire the entire share capital of BHP Petroleum International Pty Ltd (BHP Petroleum) in exchange for new Woodside shares.

On completion of the merger, Woodside will issue new shares expected to comprise approximately 48% of all Woodside shares as consideration for the buyout of BHP Petroleum. Woodside plans to put the agreed $28 billion merger to a vote in the second quarter of 2022.

If completed, the merger will create a global top 10 independent energy company by production and the largest energy company listed on the Australian Securities Exchange. The combined business will have a high-margin oil portfolio and long-life LNG assets. Estimated synergies of more than $400 million per annum are expected, via optimizing corporate processes and systems, leveraging combined capabilities and improving capital efficiency on future growth projects and exploration. The combined entity will have a strong growth profile with shared values and a focus on sustainable operations. It will have increased financial resilience, compared to BHP’s and Woodside’s standalone petroleum businesses.

Image Source: Zacks Investment Research

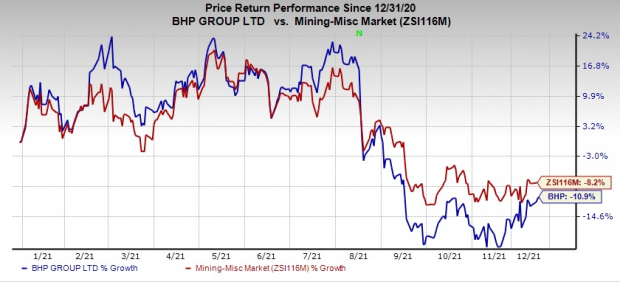

BHP’s shares have fallen 10.9% so far this year, compared with the

industry

’s decline of 8.2%.

BHP’s share price has borne the brunt of the plunge in iron ore prices witnessed earlier this year. Iron ore demand had taken a hit on the intensified curbs on steel production in China that in turn impacted prices of the steel-making ingredient. However, iron ore prices have recently picked up on supply constraints and prospects of improving demand in China. China’s steel mills are anticipated to increase production as some companies completed crude steel output reduction targets. China’s property sector is also showing signs of improvement. This is likely to support iron ore prices. Copper prices have gained lately amid signs of an improvement in China’s real estate sector. This scenario bodes well for BHP.

The company will gain on its ongoing efforts to make operations more efficient through smart technology adoption across the entire value chain and focus on lowering debt. Exit of the petroleum business, investment in growth projects and decision to unify its dual-listed structure will drive growth for the company as well.

Zacks Rank & Key Picks

BHP currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks from the basic materials space are

AdvanSix Inc.

ASIX

,

Celanese Corporation

CE

and

The Chemours Company

CC

. While ASIX flaunts a Zacks Rank #1 (Strong Buy), CE and CC carry a Zacks Rank #2 (Buy). You can see

the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

.

AdvanSix has a projected earnings growth rate of 194.5% for the current year. The Zacks Consensus Estimate for earnings for the current year has been revised upward by 5.9% over the last 60 days.

AdvanSix beat the Zacks Consensus Estimate for earnings in each of the trailing four quarters, the average being 46.9%. ASIX has rallied around 125% so far this year.

Celanese has an expected earnings growth rate of 139.5% for the current year. The Zacks Consensus Estimate for current-year earnings has been revised upward by 8.7% in the past 60 days.

Celanese beat the Zacks Consensus Estimate for earnings in each of the last four quarters, the average surprise being 12.7%. The stock has surged around 23% so far this year.

Chemours has an expected earnings growth rate of 105.1% for the current year. The Zacks Consensus Estimate for earnings for the current year has been revised upward by 10% in the past 60 days.

Chemours beat the Zacks Consensus Estimate for earnings in the last four quarters. The company has a trailing four-quarter earnings surprise of roughly 34.2%, on average. It has appreciated around 31.5% year to date.

Infrastructure Stock Boom to Sweep America

A massive push to rebuild the crumbling U.S. infrastructure will soon be underway. It’s bipartisan, urgent, and inevitable. Trillions will be spent. Fortunes will be made.

The only question is “Will you get into the right stocks early when their growth potential is greatest?”

Zacks has released a Special Report to help you do just that, and today it’s free. Discover 5 special companies that look to gain the most from construction and repair to roads, bridges, and buildings, plus cargo hauling and energy transformation on an almost unimaginable scale.

Download FREE: How to Profit from Trillions on Spending for Infrastructure >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report