Central banks are dumping dollars and stockpiling gold at the fastest rate in decades. China just slashed its Treasury holdings to a 17-year low while extending its gold-buying spree for 13 consecutive months. Tether has quietly amassed 116 tonnes of physical bullion. And Goldman Sachs is now calling for $5,400 gold by Q4 2026.

The institutional exodus from paper assets into hard money is accelerating. And the smart money isn’t just buying bullion. They’re hunting for gold producers that can capture this once-in-a-generation move.

Here’s the problem. There aren’t enough of them.

New mine supply is growing at just 1% annually. Most development projects won’t pour their first ounce until 2030 or later. The supply squeeze is real.

That’s what makes Norsemont Mining Inc. (CSE:NOM) (OTC:NRRSF) so compelling right now.

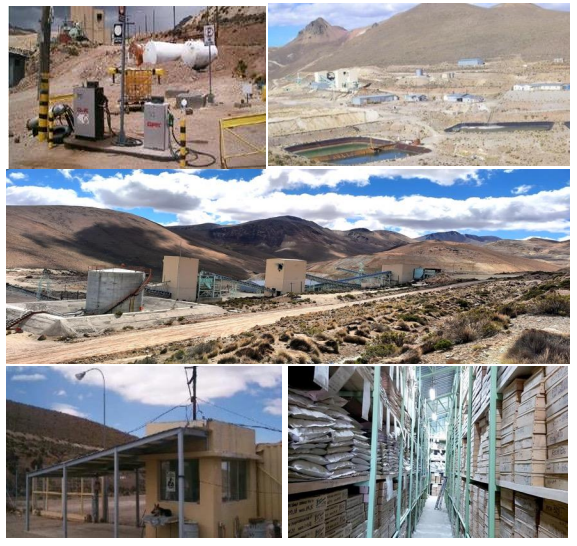

They’re not building a mine from scratch. They acquired one. A past-producing Chilean operation called Choquelimpie that Shell built in the 1980s and abandoned when gold was under $400 per ounce.

The gold never left. The infrastructure never disappeared. And now, with gold hovering around the $5,000 per ounce mark, Norsemont is racing to bring it back online.

Production target: 2027.

On 30,000 ounces annually, you’re looking at potential operating cash flow approaching $135 million per year.

And the stock? Trading at roughly $96 million market cap. That’s less than $40 per ounce for 2.18 Million indicated and 557,000 inferred gold-equivalent ounces sitting in the ground.

Why the Smart Money Is Quietly Loading Up on This Name

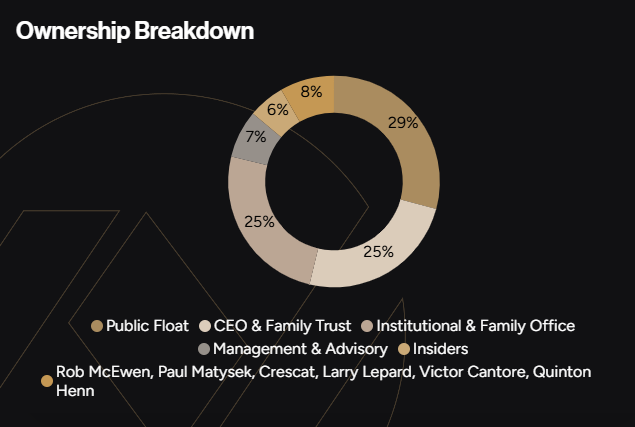

When Rob McEwen, Paul Matysek, Quinton Hennigh, and Crescat Capital all start buying the same junior gold stock, it’s worth paying attention.

These aren’t momentum chasers. McEwen built Goldcorp into one of the most successful gold companies in history. Matysek has sold multiple mining companies for billions. Hennigh built his reputation finding undervalued gold assets before the crowd arrives.

Norsemont Mining (CSE:NOM) (OTC:NRRSF) has raised over $21 million from strategic investors alone., No brokers. No hedge funds. Every dollar came from people who have done the due diligence.

And here’s the signal that matters most. Crescat increased its position at a higher price in December. Sophisticated funds don’t average up unless they see something big coming.

CEO Marc Levy has $10 million of his own money in this deal. That’s roughly 21% ownership of the entire company. When did you last see that kind of alignment in a junior?

Add it up and 38% of the shares are held by insiders and strategic investors. The float is tight. When broader attention arrives, there won’t be much stock available.

The Asset: Hundreds of Million in Infrastructure That Most Juniors Spend a Decade Building

Between 1988 and 1992, Shell extracted over 398,900 ounces of gold and 2.19 million ounces of silver from Choquelimpie. It was Chile’s third-largest gold producer.

Then gold crashed below $400. They walked away.

But they left behind everything. A 3,000 tonne-per-day mill. Power connected to the grid. Water permits. Year-round road access. Camp facilities. Over 2,000 drill holes, for 143,047 meters of drilling.

Norsemont Mining Inc. (CSE:NOM) (OTC:NRRSF) didn’t spend years exploring or hundreds of millions building. They stepped into a turnkey operation worth $175 million in replacement value.

Mineral Resource Estimate (March 31, 2025)

| Category | Tonnes (M) | Au (g/t) | Ag (g/t) | Cu (%) | AuEq (g/t) | AuEq Ounces |

| Indicated | 81.89 | 0.66 | 12.62 | 0.04 | 0.83 | 2,184,000 |

| Inferred | 25.27 | 0.55 | 8.89 | 0.04 | 0.69 | 557,000 |

Over 80% sits in the higher-confidence Indicated category. This isn’t speculative. It’s drilled, tested, and validated by actual production.

The 33.2 indicated and 7.2 inferred million ounces of contained silver at today’s $80+ prices provides meaningful economic uplift on every tonne mined.

And the drill intercepts Shell left behind are stunning:

| Zone | Hole ID | Interval (m) | Au (g/t) | Ag (g/t) |

| Vizcacha | A-327 | 35.0 | 30.5 | 8.0 |

| Vizcacha | A-417 | 22.0 | 13.70 | 3.34 |

| Choque | R-002 | 158.0 | 3.90 | 200.0 |

| Choque | R-066 | 120.0 | 4.10 | 252.0 |

| Suri | R-579 | 24.0 | 35.10 | 137.0 |

| Suri | R-554 | 58.0 | 6.40 | 167.0 |

That Vizcacha hit represents over 1,100 gram-meters. Anything above 100 is significant. Above 1,000 is world-class. Norsemont (CSE:NOM) (OTC:NRRSF) has 59 intercepts exceeding 100 gram-meters already in their database.

The Path to Production: 18 Months, Not 10 Years

Most developers quote $500 million to $1 billion in construction capital and timelines stretching past 2030.

Norsemont Mining (CSE:NOM) (OTC:NRRSF) is targeting first pour in 2027 with $10 to $25 million in restart capex.

The plan is straightforward. Start with the oxide material that Shell successfully heap-leached decades ago. There’s already 196,000 ounces of gold sitting in stockpiles on site that were sub-economic at $400 gold but highly profitable at $5,000. Combined with additional shallow oxide resources, management is targeting 1.0 to 1.5 million ounces to feed the initial operation.

The Environmental Impact Assessment is underway in a region that actively wants mining. Government officials have told Norsemont directly they support the project. Review periods typically run 6 to 12 months.

Once cash flow starts, Norsemont Mining Inc. (CSE:NOM) (OTC:NRRSF) self-funds expansion into the 1.6 million additional ounces in mixed and sulfide material. No dilutive raises. No handing upside to investment banks.

Press Releases

- Norsemont Resumes Phase Three Drill Program at Choquelimpie

- Norsemont Commences Trading on the OTCQX Market

- Norsemont Targets Filing Environmental Impact Declaration In December 2026

- Norsemont Drills 94 meters at 1.26 g/t Au and 109 meters at 1.09 g/t Au Both Holes Starting at Surface

- They Acquired a $175+ Million Mine. Now They’re Bringing It Back Online Just as Gold Tests $5,000

The Upside the Market Isn’t Pricing: 7.5M Oz Resource + Copper Porphyry

Here’s what most investors miss.

Shell’s drilling averaged just 70 meters in depth. But high-sulfidation epithermal systems like Choquelimpie typically extend to 300 meters or deeper. They stopped drilling while still in ore.

Management believes the resource can grow from 2.18 million indicated and 557,000 inferred gold-equivalent ounces to 7.5 million ounces or more by simply drilling deeper into zones already defined at surface. The Phase 3 program is testing exactly this with 20 diamond holes targeting 300-meter depths.

And then there’s the copper.

In 2021, Norsemont hit 170 meters grading 1.35 g/t gold and 0.2% copper at depth, with copper grades increasing to 0.7% to 1.1% before they stopped drilling. Geologists recognized it immediately. They’d hit the top of a copper porphyry system.

Dr. Sergei Diakov, who led the team that discovered the massive Oyu Tolgoi deposit, joined Norsemont Mining (CSE:NOM) (OTC:NRRSF)‘s board specifically for this porphyry potential. Management believes this could be a 500 million to 1 billion tonne target.

The market is assigning zero value to any of this. If the porphyry proves out, this becomes a completely different story.

The Valuation Gap Is Glaring

Industry rule of thumb: development-stage ounces trade at $100/oz in good jurisdictions with quality assets.

Norsemont Mining Inc. (CSE:NOM) (OTC:NRRSF) has 2.18 Million indicated and 557,000 inferred gold-equivalent ounces. At $100/oz, that’s $274 million implied value.

Current market cap? ~$96 million. That’s less than $40/oz.

Rio2 Limited mines gold in Chile at lower grades with a market cap of $1.75 billion. They raised hundreds of millions to build their operation. Norsemont is targeting production with a tiny capex because the infrastructure already exists.

The market is pricing zero value for the resource expansion to 7.5M oz. Zero for the copper porphyry. Zero for the 196,000 oz of gold in stockpiles. Zero for silver credits at $80+.

Gaps like this close two ways. Either the market wakes up. Or someone writes a check and takes the asset at a premium.

A Team That’s Done This Before At Billion-Dollar Scale.

Marc Levy built the original Norsemont from $1M market value to a $520M sale to Hudbay. He’s been involved in over $1 billion in mining exits and co-founded Aurora Cannabis (peaked at $16B valuation).

Mijael Thiel built the $2.7 billion Esperanza project in Chile, taking it from the first drill hole to production in six years, on time and on budget.

David Laing literally put Choquelimpie into production for Shell in the 1980s. He later became CEO of Equinox, True Gold, and Quintana, and advised on $25 billion in mining M&A. When Norsemont Mining (CSE:NOM) (OTC:NRRSF) acquired the project, Levy called Laing to come back. He said yes.

2026 Catalyst Calendar

- Q1: Phase 3 drilling results (7 deep holes, assays pending)

- Q1-Q2: Metallurgical testwork results

- Q2: Engineering study with detailed capex

- Q2-Q3: Updated NI 43-101 resource estimate

- Q3: Preliminary Economic Assessment

- Q3-Q4: Results from the balance of the Phase 3 and the Oxide Expansion drill holes.

- Q3-Q4: Environmental Impact Assessment submission

Six major catalysts. Twelve months. Each one capable of re-rating the stock.

One of Those Rare Moments Where This Kind of Setup Doesn’t Stay Cheap For Long

A past-producing mine with 2.18 Million indicated and 557,000 inferred gold-equivalent ounces in the ground. $175M in existing infrastructure. Production targeted for 2027. Resource expansion potential to 7.5Moz to 9Moz. A copper porphyry the market isn’t pricing in. Billionaires and legendary mine builders already on the register. A CEO with $10M of his own capital invested.

All trading at less than $40/oz while gold tests $5,000.

Norsemont Mining Inc. (CSE:NOM) (OTC:NRRSF) isn’t crowded yet. But the smart money has found it. The question is whether you’ll look before or after the re-rating happens.

Click here to download Norsemont Mining’s investor presentation.