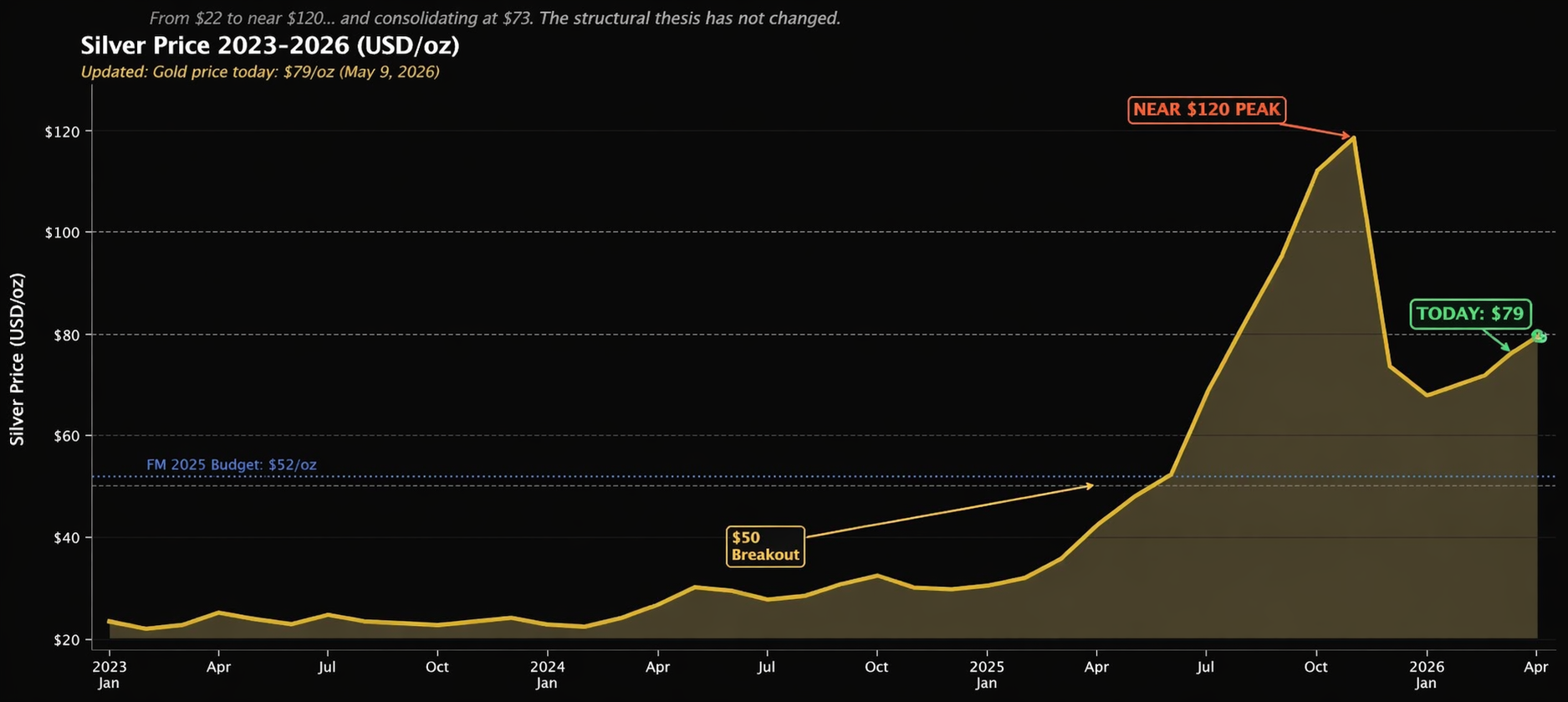

Silver broke through $100/oz for the first time in years. Then $110. Then nearly $120.1

The bulls who had been calling for triple-digit silver were finally right. The skeptics went quiet. And investors who had been waiting for confirmation got it in a way nobody could argue with.

Then came the pullback. Silver dropped sharply from the peak. It found a floor around $65, bounced, and has been consolidating in the $70 to $80 per ounce range ever since.

Here is what the pullback did not change.

The world is still running a structural silver deficit for the fifth consecutive year.2 Industrial demand is growing faster than mines can supply. AI data centers are consuming silver at a rate that was not in any forecast two years ago. Powering just one major data center requires a 500-megawatt solar array, which alone consumes around 300 metric tons of silver.3 Solar demand hit a new record in 2024. China is still restricting silver exports and stockpiling what it buys from North America.4

The fundamental story that drove silver from $22 to $120 did not evaporate when the price pulled back. The supply-demand math is intact.

Which brings up a more interesting question. If the next move higher does come… who is positioned best to benefit?

The answer is First Majestic Silver Corp. (NYSE:AG) (TSX:AG).

And the case for looking at it carefully right now is built on something more durable than momentum. It is built on cash. On production. On margin. On a balance sheet that most investors have no idea is this strong.

Breaking News

A Mining Company With $938 Million in Cash Is Not Something You See Every Day

First Majestic Silver Corp. (NYSE:AG) (TSX:AG) ended 2025 with a treasury of $937.7 million,5 cash and equivalents at the highest level in company history.

This is a company trading around $10 billion in market cap. That means roughly 9 cents of every dollar you pay for the stock is backed by cash sitting in the bank right now. Before counting the mines. Before counting the ounces in the ground. Before counting the minting facility or the restart of their gold mine in Nevada.

How did they accumulate nearly a billion dollars?

By having the best financial year in company history.

The actual treasury figure came in at $937.7 million.6 He was right to be excited.

What does nearly $1 billion in cash do for a silver company?

Three things.

First: it provides a floor. If silver drops again, First Majestic Silver Corp. (NYSE:AG) (TSX:AG) weathers it without diluting shareholders.

Second: It allows the company to internally fund its own growth initiatives like the mine expansion at Los Gatos, the mill expansion at Santa Elena and the restart at Jerritt Canyon without going to market with hat in hand.

Third: it enables opportunistic acquisitions to add additional ounces on an accretive basis to existing shareholders.

It signals operational discipline. You do not accumulate a treasury this large by accident. You do it with a relentless focus on costs and margins. The cash is real, not paperfunded by debt.

The Budget Was $52 Silver. The Metal Is at $79. Every Dollar in Between Is Unplanned Margin

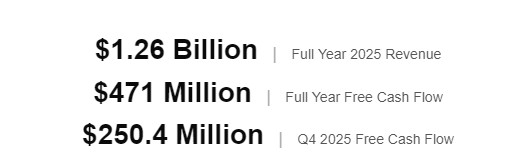

First Majestic Silver Corp. (NYSE:AG) (TSX:AG) planned its entire 2026 budget at a silver price of $52 per ounce.7 Last year, the average realized selling price for the full year was $41.52. And they still generated $471 million in free cash flow.

Silver is now at $79. That is $21 per ounce above the budget level. On approximately 13 to 14.4 million silver ounces of annual production, that gap represents significant unplanned margin flowing directly to the bottom line. And that doesn’t even include the up to 129,000 ounces of gold that the company expects to produce in 2026.

Q1 2026 financial results are scheduled for May 12, 2026, the same day First Majestic will announce its Q1 dividend under a new policy that doubles the payout to 2% of revenue, up from 1% previously.8 It’s also the first quarter to fully reflect silver at $70+ rather than the $55 average that drove Q4’s record $250.4 million in quarterly free cash flow.9

When those numbers land, investors using old models will need to update their thinking.

“We did our budget at $52 silver. Seeing it at $70 means we are exceeding our baseline. That is great for us.” – Mani Alkhafaji, President, First Majestic Silver

The all-in sustaining cost across the portfolio was approximately $21 per silver equivalent ounce in 2025.10

At $79 silver, the realized margin before corporate overhead is roughly $52 per ounce.

First Majestic’s (NYSE:AG) (TSX:AG) lowest-cost mine, Los Gatos, ran at just $15.15 All-In Sustaining Cost (AISC) per ounce in 2025,11 nearly a five-to-one margin at that single asset.

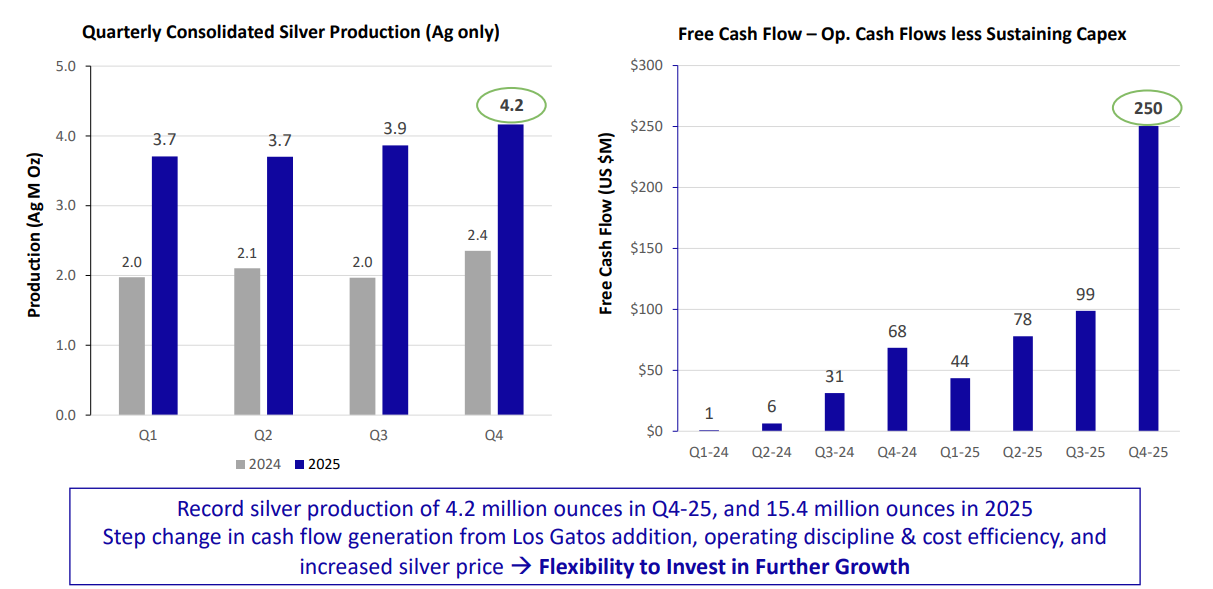

The trajectory above tells the story. From $1 million in quarterly free cash flow in Q1 2024 to $250.4 million in Q4 2025.12

That is a step change, not an incremental improvement. Driven by the Los Gatos acquisition, operational discipline across all mines, and a silver price that finally started reflecting structural reality.

Press Releases

- First Majestic Announces Restart Plan for Jerritt Canyon Gold Mine

- First Majestic Announces 2025 Mineral Reserve and Mineral Resource Estimates

- First Majestic Announces Results of the 2025 Drilling Program at Jerritt Canyon Gold Mine

- First Majestic Reports Q4 2025 and Full Year 2025 Financial Results; Announces Quarterly Dividend Payment

- First Majestic Reports Positive Exploration Results at Los Gatos

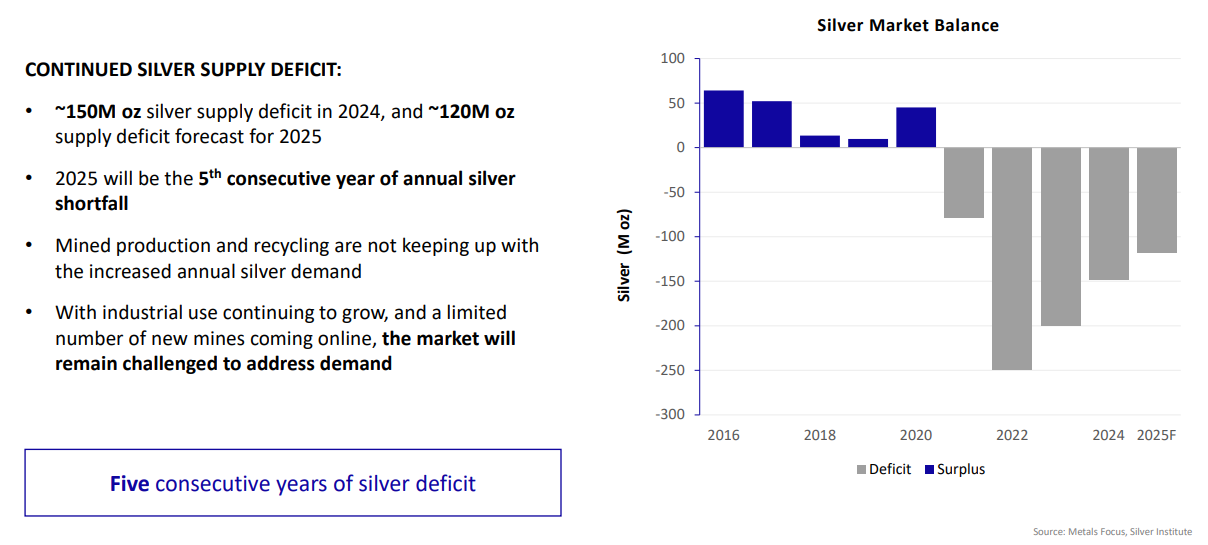

Five Consecutive Years of Silver Deficit. And the New Demand Drivers Are Not Even Fully in the Models Yet

For five consecutive years, the world has consumed more silver than it has produced.13

In 2024 alone, the global silver market ran approximately 150 million ounces short, or about 10 times First Majestic’s annual production. The 2025 estimate is another 120 million ounce shortfall. This is not a temporary disruption. This is a structural imbalance.

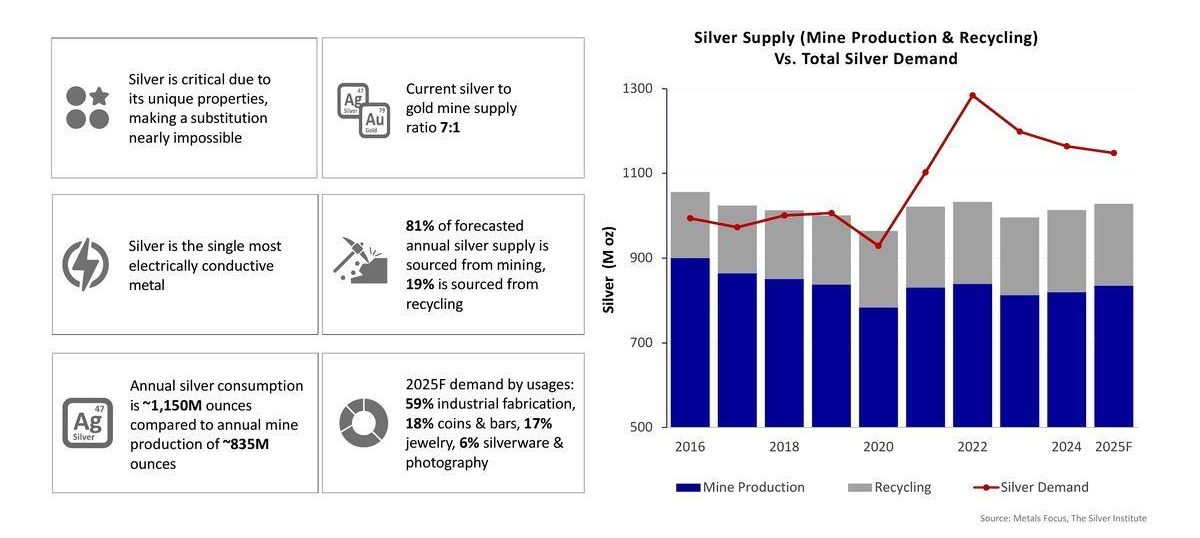

The biggest driver is solar energy. Silver paste is used in approximately 90% of all crystalline silicon photovoltaic cells. Solar demand for silver hit a record 198 million ounces in 2024, a 140% increase since 2020.14 One industry. A quarter of total annual silver mined.

Then there are the demand drivers that are not fully priced into forward models. AI data centers are estimated to require several thousand ounces of silver across their servers, connections, and cooling systems, with AI server clusters carrying two to three times the silver content of conventional facilities. Solid-state battery technology from manufacturers like Samsung uses approximately one kilogram of silver per cell. Nuclear energy’s return as a politically accepted clean power source adds another new demand category.

None of these were meaningfully in the five-year Silver Institute demand forecast when it was originally published.

On the supply side, approximately 70% of all silver produced globally is a byproduct of copper, gold, and zinc mining.15 Those mines respond to the economics of their primary metal, not silver. When silver runs, byproduct supply does not increase proportionally. And primary silver mines like the ones First Majestic Silver Corp. (NYSE:AG) (TSX:AG) operates take seven to fifteen years to develop from discovery to production. The deficit is not closing.

The Most Silver-Pure Major Producer on Earth. Here Is What That Actually Means

Not every silver company is built the same way. Some produce silver as an afterthought alongside gold or copper. Some carry heavy debt. Some operate in jurisdictions that create discount risk no silver price can fully offset.

First Majestic Silver Corp. (NYSE:AG) (TSX:AG) was built from the ground up with a single mission: to be the world’s leading primary silver producer. The revenue structure reflects that.

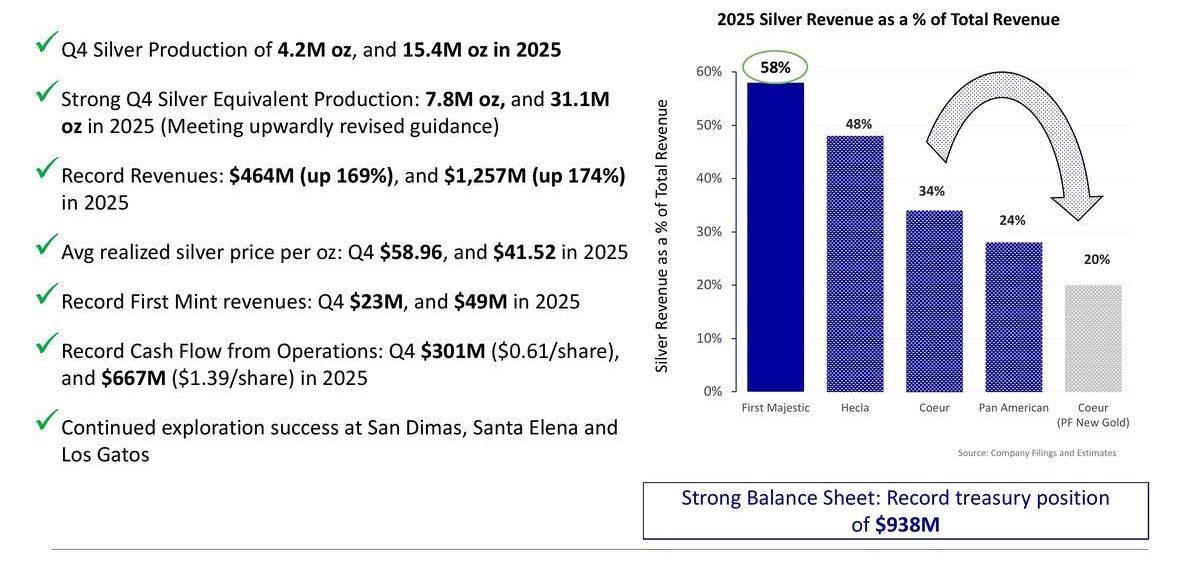

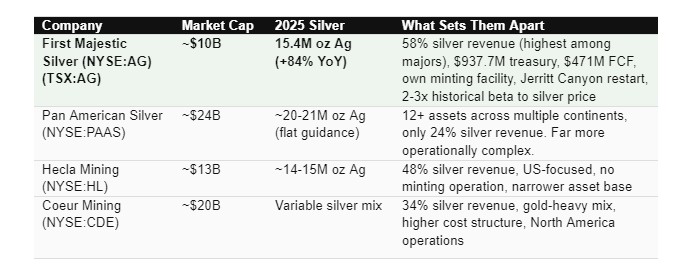

58% of revenue comes from silver. 90% from precious metals total.16

Among all the major producers, that is the highest silver concentration by revenue. When silver moves, First Majestic (NYSE:AG) (TSX:AG) moves with it more directly than any of its peers. Historically, the company has delivered a 2 to 3x beta to the silver price over the full cycle.17

Here is how the major producers compare on silver revenue purity: First Majestic Silver Corp. (NYSE:AG) (TSX:AG): 58%, Hecla Mining: 48%, Pan American Silver (NYSE:PAAS): 24%, Coeur Mining: 34%.18

Pan American has more total silver production but only 24% of its revenue is silver. Three quarters of what drives Pan American’s earnings is everything other than silver. For an investor who wants silver exposure, that is a significant dilution of the thesis.

First Majestic Silver Corp. (NYSE:AG) (TSX:AG) is the concentrated position. Not a diversified miner that happens to produce some silver.

Four Mines. Four Active Operations. Each Adding a Different Layer to the Story

With four active operations and a funded restart in motion, First Majestic Silver Corp. (NYSE:AG) (TSX:AG) has built a multi-mine portfolio where each asset adds a different layer of scale, margin, exploration upside, and production leverage.

In Q1 2026 alone, the company completed nearly 66,000 metres of drilling across its four mines, with up to 27 rigs running simultaneously.19 That is not exploration for exploration’s sake, it is a systematic program to grow the reserve base faster than production depletes it.

Los Gatos: The Lowest-Cost Asset That Changed the Company’s Scale

For First Majestic Silver Corp. (NYSE:AG) (TSX:AG), Los Gatos is not just a new mine.It is the asset that transformed the company’s financial profile, and the numbers back that up at every turn.

The January 2025 Gatos Silver acquisition was the largest transaction in First Majestic history at $970 million. Within a single year, it had fundamentally reshaped what kind of company First Majestic is.

Annual revenue increased by 174% to a record $1.26 billion in 2025 and free cash flow reached $470.6 million for the year. The $970 million price tag, once questioned by skeptics, has essentially been validated by one to two years of operational cash flow.

Los Gatos in Chihuahua, Mexico is one of the highest-grade silver mines in the Western Hemisphere. In its first full year under First Majestic’s (NYSE:AG) (TSX:AG) ownership, it delivered 8.4 million ounces of silver at an all-in sustaining cost of $15.15 per ounce,20 nearly a five-to-one margin at $79 silver.

Throughout 2025, Los Gatos contributed approximately one-third of the company’s total production, delivering 1.5 million attributable ounces of silver per quarter by year-end.

The growth story is far from over. The mine sits on 103,000 hectares of exploration ground, 85% of which has never seen a drill. A 61,000 metre exploration program is planned for 2026 targeting expansion of the Central and Northwest Deep zones, alongside plans to increase mill throughput to 4,000 tonnes per day.21

Q1 2026 confirmed the ramp-up is real. Los Gatos processed 227,379 tonnes in the quarter, up 17% year-over-year, at a head grade of 190 g/t silver, delivering 1.18 million ounces.22

Management has set a specific target of 4,000 tpd in the second half of 2026. Five drill rigs are running continuously at the Central and Northwest Deeps zones. The mine is not yet at full speed.

San Dimas: 250 Years of History. Still the Cornerstone.

For First Majestic Silver Corp. (NYSE:AG) (TSX:AG), San Dimas remains a cornerstone asset with both production weight and long-term exploration depth and recent results suggest the best may still be ahead.

First reported mining activity in the San Dimas district dates back more than 250 years.23 Historical production from the district is estimated at over 11 million ounces of gold and 750 million ounces of silver.

Yet extensions of historically mined areas remain untested by modern methods across the mine’s 71,867-hectare land package, a detail that helps explain why First Majestic Silver continues to direct its largest share of exploration capital here.

In 2025, the company’s full year production totalled 31.1 million silver equivalent ounces, including 15.4 million ounces of silver and 147,433 ounces of gold,24 with production at San Dimas totalling 10.2 million silver equivalent ounces, increasing 19% year-over-year and representing 33% of First Majestic’s total production.

The exploration pipeline continues to deliver. Recent Perez vein drilling at San Dimas returned intercepts as high as 10.87 g/t gold and 1,034 g/t silver over 7.88 metres, with the vein still open in both directions.25 A new Coronado vein discovery announced in August 2025 adds further resource upside to an already substantial base.26

Notably, proven and probable reserves across First Majestic‘s Mexican operations grew 4% to 184.8 million silver-equivalent ounces as of December 31, 2025, despite active depletion,27 underscoring the effectiveness of the company’s drill-to-replace strategy.

With approximately 50% of its power sourced from clean hydroelectricity, San Dimas also carries a structural cost advantage over diesel-powered peers, making it as efficient as it is prolific.

Two and a half centuries in, San Dimas is still delivering.

Santa Elena: Two New Discoveries. Both Within 900 Metres of the Plant.

Santa Elena runs the first High-Intensity Grinding mill deployed in the silver industry. This technology micronizes ore into ultra-fine slurry rather than crushing it with steel balls, achieving significantly higher metal recovery rates per tonne processed.

The bigger story is what the drills have found nearby. The Navidad vein system was discovered in July 2024 less than two kilometres from the plant, with metallurgical recoveries exceeding 95% for both gold and silver.28

Then in May 2025, First Majestic Silver Corp. (NYSE:AG) (TSX:AG) made a second discovery at Santo Nino, just 900 metres from the plant, a large epithermal vein traced over one kilometre of strike and 400 metres down-dip across a 32-hole drill program, with mineralization still open to the east.29

That work has now produced a declared resource. Navidad and Santo Niño together host 10.5 million tonnes Inferred containing 90.7 million silver-equivalent ounces at an average grade of 268 g/t AgEq.30

Two discoveries. Both with close proximity to an operating plant with industry-leading recovery technology already in place.

In Q1 2026, seven drill rigs completed 20,429 metres of drilling at Santa Elena, with infill drilling actively converting Inferred resources to Indicated. The resource is not static. It is being upgraded quarter by quarter. Most analyst models have not yet reflected these ounces.

La Encantada: Pure Silver. Full Stop.

Within the First Majestic Silver Corp. (NYSE:AG) (TSX:AG) portfolio, La Encantada remains the clearest single-asset expression of the silver thesis.

La Encantada only produces silver. No gold, no base metals. It is the cleanest single-metal expression of the silver thesis within the portfolio.

In Q4 2025, production hit 1 million ounces, up 32% year-over-year and 74% over the prior quarter.31 At $79 silver, every recovered ounce is pure margin expansion with no byproduct math to complicate it.

Jerritt Canyon, Nevada: The Funded Restart That Is Not Yet in the Stock Price

On April 2, 2026, First Majestic Silver Corp. (NYSE:AG) (TSX:AG) committed $75 million to support the restart of its fully permitted Jerritt Canyon Gold Mine in Elko County, Nevada.32

The money is committed, infrastructure in place, the engineering firm is hired, and the physical work has already started.

Stantec Consulting Services, one of the largest infrastructure and engineering firms in North America, has been engaged to complete a pre-feasibility study due Q4 2026. Rehabilitation of the Smith and SSX underground mines commenced in Q2 2026. Processing plant upgrades are underway, a new water supply well is under construction, and mining fleet procurement has begun.

This is not a plan on paper. It is an active restart.

The resource base: 4.1 million ounces of gold in Measured and Indicated categories, plus 3.7 million ounces Inferred, as of December 31, 2025.33 Updated resource estimates flagged the asset’s strong sensitivity to bulk-tonnage, low-cost open-pit mining, a more compelling economic profile than a pure underground operation.

The 2026 program includes 42,000 metres of drilling to further define that open-pit potential alongside underground development at Smith-SSX.

Jerritt Canyon is also one of only three permitted gold processing facilities in Nevada using roasting technology, a critical and essentially irreplaceable advantage for the refractory ore on site.

First Majestic has flagged July 2026 as the date for its H2 guidance update, which will include the revised Jerritt Canyon capital budget and, possibly, initial production targets. The pre-feasibility study is due Q4 2026. Production is targeted for H2 2027.34

Most analyst models do not yet include Jerritt Canyon production. When they update, the valuation math changes because at $4.700/oz gold, there is lots of margin and cash flow to be had.

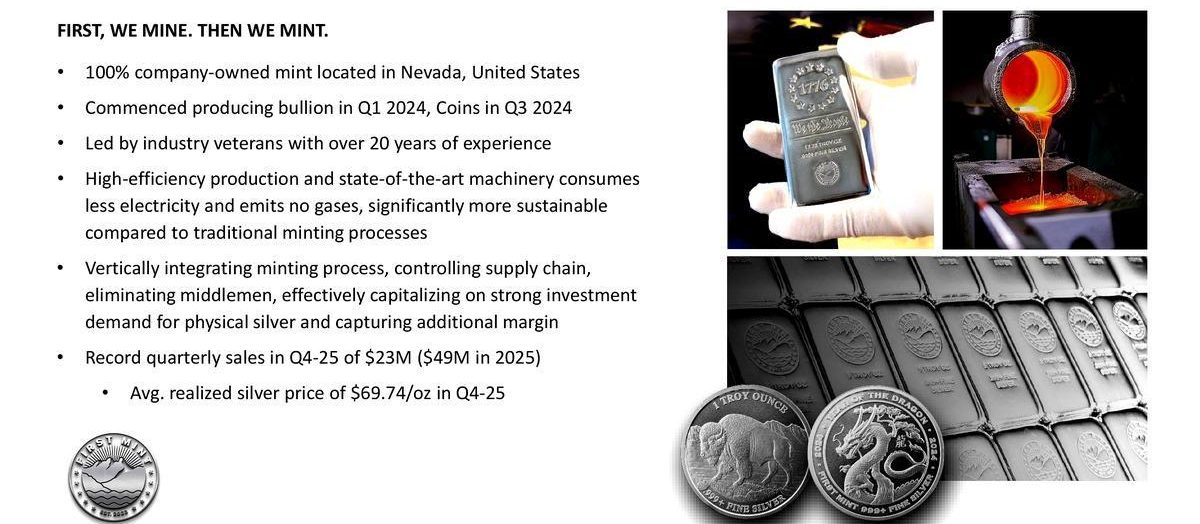

The Only Miner on Earth That Mints Its Own Metal and Keeps the Premium

First Majestic Silver Corp. (NYSE:AG) (TSX:AG) is the only publicly traded mining company in the world with its own minting facility. Instead of selling all silver at or near spot price, it mints bars, coins, and rounds and sells them directly to retail buyers through FirstMint.com at retail premiums.

First Majestic Silver Corp. (NYSE:AG) (TSX:AG) is the only publicly traded mining company in the world with its own minting facility. Instead of selling all silver at or near spot price, it mints bars, coins, and rounds and sells them directly to retail buyers through FirstMint.com at retail premiums.

The Q4 2025 results: COMEX silver averaged $55.20 per ounce. First Mint realized an average selling price of $69.74 per ounce, a 26% premium.35 In just its second year of operation, full year 2025 First Mint revenue was $49.4 million with operating earnings of $24.1 million.

Apple designed its own chips to remove dependencies and capture additional margin. First Majestic Silver Corp. (NYSE:AG) (TSX:AG) built its own mint to capture the premium that every other miner leaves on the table.

Same logic. Different industry. No competitor has copied it.

“The mint generated about $50 million of revenue with about a 50% gross margin. That is a margin profile that many pure mining companies don’t have.” — Mani Alkhafaji, President, First Majestic Silver

Why This Specific Moment Is Worth a Second Look

The silver thesis has been building for years. What makes right now a particularly interesting time to take a careful look?

The $120 moment changed sentiment permanently. When silver briefly touched triple digits earlier this year, the credibility of the bull case was established. The pullback to $79 has not restored skepticism. It has created a waiting period. Investors who missed the first move are watching for the next entry.

Q1 2026 earnings will be the first to fully reflect current silver prices. Q4 2025 free cash flow of $250.4 million was generated when silver averaged $55.36 Q1 2026 will show what the machine generates at $70+. Those numbers are coming on May 12, 2026, alongside the Q1 dividend announcement.

Two Santa Elena discoveries now have declared resources and most analyst models still do not include them. Navidad and Santo Niño together host 90.7 million silver-equivalent ounces Inferred at 268 g/t AgEq. That gap between what is in the ground and what is in the models is exactly the kind of dislocation that gets repriced.

Jerritt Canyon is a funded catalyst with a defined timeline. $75 million committed, pre-feasibility due Q4 2026, production targeted H2 2027.37 Most models do not yet include this. When they do, the math changes.

The dividend just doubled and it scales with silver. The 2026 policy targets 2% of net quarterly revenues per share, up from 1% previously.38 As silver prices rise and revenue grows, the dividend grows with it. That is a new category of investor who has a reason to look.

None of these factors individually tells you what the stock will do. But together they form a picture of a company with strong fundamentals, multiple near-term catalysts, and a macro tailwind that has not run its course.

The World Is Being Rewired Around Silver. And That Changes the Supply Math

The geopolitical backdrop to this silver story is not incidental. It is structural.

Russia and Ukraine remain at war. The Middle East is in open conflict. China and the US have moved from trade rivalry to outright economic confrontation. In this environment, every major economy is rethinking where it sources critical materials.

The US officially designated silver a critical mineral in 2025,39 placing it alongside copper and rare earths in terms of national security importance. That designation unlocks federal programs: prioritized permitting, potential government stockpiling, and domestic sourcing preferences in procurement contracts.

China controls most of the world’s silver smelting capacity for concentrates. Silver concentrate from North America and South America travels to Asian smelters for processing. Increasingly, that silver is staying in China. Beijing is paying premiums to acquire it.40 What leaves does not come back.

North America has no silver concentrate smelters at commercial scale. The US has signaled interest in building one. The timeline: billions of dollars and seven to eight years. In the meantime, the supply available to Western markets is tightening in a way that is structural, not cyclical.

First Majestic Silver Corp. (NYSE:AG) (TSX:AG) operates in Mexico with free trade agreements covering the US, Canada, and the European Union.

It sells directly into the US market through its Nevada-based First Mint facility. And 22 years of operational history in Mexico gives it relationships and institutional knowledge that no new entrant can replicate quickly.

In a world where supply chains are being rewired, proximity, established licensing, and operational track record matter enormously. First Majestic (NYSE:AG) (TSX:AG) has all three.

The Smart Money Is Already Here. 60% Institutional Ownership Says It All

60% of First Majestic Silver Corp. (NYSE:AG) (TSX:AG) shares are held by institutions.41

Van Eck (GDX/GDXJ) is the largest holder at 8.4%. Tidal Investments (SILJ) holds 5.0%. Global X (SIL) holds 3.8%. Vanguard 2.3%. Blackrock 1.6%.42

Every major silver-focused ETF owns First Majestic as a core holding. These are not speculative positions. They are informed, researched, actively managed stakes in a company that these funds have evaluated in depth.

Six analyst firms cover the stock: Bank of Montreal, Scotiabank, TD Cowen, H.C. Wainwright, Cormark Securities, and National Bank Financial.43

Average daily trading volume across NYSE and TSX exceeds $400 million combined.44 That is institutional-grade liquidity. Large capital can move in and out efficiently.

The professionals have already run the analysis. They looked at the $937.7 million treasury, the $471 million in free cash flow, the Santa Elena discoveries, and the Jerritt Canyon restart. They own the stock. That context is worth having.

The Numbers Are Built. The Story Is Real. The Ounces Are Coming Out of the Ground Right Now

Silver touched $120.

The pullback happened. The consolidation is real. And the structural deficit that drove the move is still running, deepening, and adding new demand categories that were not in anyone’s model when this bull market began.

First Majestic Silver Corp. (NYSE:AG) (TSX:AG) sits at the center of this story with $937.7 million in cash, four producing mines, the world’s only miner-owned minting facility generating retail premiums, a funded Nevada gold restart with a 2027 production target and a dividend that has doubled and will increase further when silver prices rise.

The company’s best financial year in history just happened at an average silver price of $41.52 per equivalent ounce. Silver is now at $79.

The machine is running. The thesis is intact. The catalysts are on the calendar.

That is worth paying very close attention to.

Subscribers to Trading Whisperer Get the Full Picture

Trading Whisperer subscribers receive our complete ongoing coverage of First Majestic Silver Corp. (NYSE:AG) (TSX:AG), including:

✔️ First Majestic’s complete April 2026 corporate presentation with all operational and financial data

✔️ Congressional trading and insider transaction monitoring for AG and all major silver names

✔️ Our proprietary AI risk scores updated in real time as market conditions change

✔️ Ongoing analysis as Q1 2026 earnings and the Jerritt Canyon pre-feasibility study become public

✔️ Real-time alerts when institutional filings signal significant new positions in the silver space

The next chapter of this silver story is being written right now.

Subscribe now to the Trading Whisperer newsletter and stay ahead of it.

*All figures are in USD unless otherwise specified